Bond Rout: Watch For Big Moves

The bond market has awoken to further inflation concerns, and bonds sold off sharply Friday—albeit a delayed reaction to recent news. Stocks followed downward

Last week, the bond market moved—but, not for the reasons you think. There is inflation, and this is cause for concern—bond markets are reacting. And, yes, last week’s moves lower in the stock market were driven by the sell off in the bond market. The only thing is, the US Treasury markets, were a reaction to the Japanese bond markets selling off sharply.

We’ve seen this before, and it was really ugly—this could be far worse.

Japan is experiencing higher inflation rates which pushed the Japanese bond markets to sell off. The US Treasury markets reacted because if there is big move lower Japanese bonds, this unwinds the carry trade. The carry trade is the FX trade that has everything to do with interest rate differentials between US & Japanese investments.

Last August, the carry trade began to unwind, and the stock market sold off sharply. This is far more serious now, and moves higher in Japanese interest rates will have crippling effects throughout the world.

This is something that I watch closely, and have done so since 1998. In that year, there were massive moves in the FX market and currency markets, and because of that,

US 30-Year Treasuries

It should be noted that the 30-year treasury yield is pushing levels it’s not seen since 2007, just prior to the financial crises (chart above). This is signaling that investors want more interest in exchange for lending to the United States government. The first reason is that with higher inflation rates, there will be higher interest rates–a likely issue that will plague world central bankers for some time. The other reason is that the deficit is moving higher, and this is further concerning investors.

Oil Prices

I do not believe that the conflict with Iran will end any time soon. I believe that a lot of the damage is already done, and that higher oil prices are here for a long time. With higher oil prices, the trickle through effects will push prices for nearly every product sold higher and higher. This will take time as the cost of higher energy prices work their way through the economy, and producers pass these costs on to consumers.

Inflation Data

The CPI was released last eek, and this saw a move higher in the Core Rate up to 2.70% year-over-year, up from 2.40%. The headline number jumped up to an increase of 3.60% year-over-year. Both of these numbers are trending back up after slowly moving lower. While it will take a few months for the higher energy costs to work their way into the core rate, it is coming.

One of the reasons, of course, for the moves higher in the core rate are tariffs. The thing to note about the tariffs and their inflation effects is that the tariffs are a purely American phenomenon. Now, however, higher energy prices will affect the entire world, and this will have a more far-reaching move in inflation prices.

Equity Markets

The equity markets paused their relentless climb higher because of the sell in the bond markets. This, too, brings in more costs for consumers because higher interest rates would affect borrowing costs for firms and consumers.

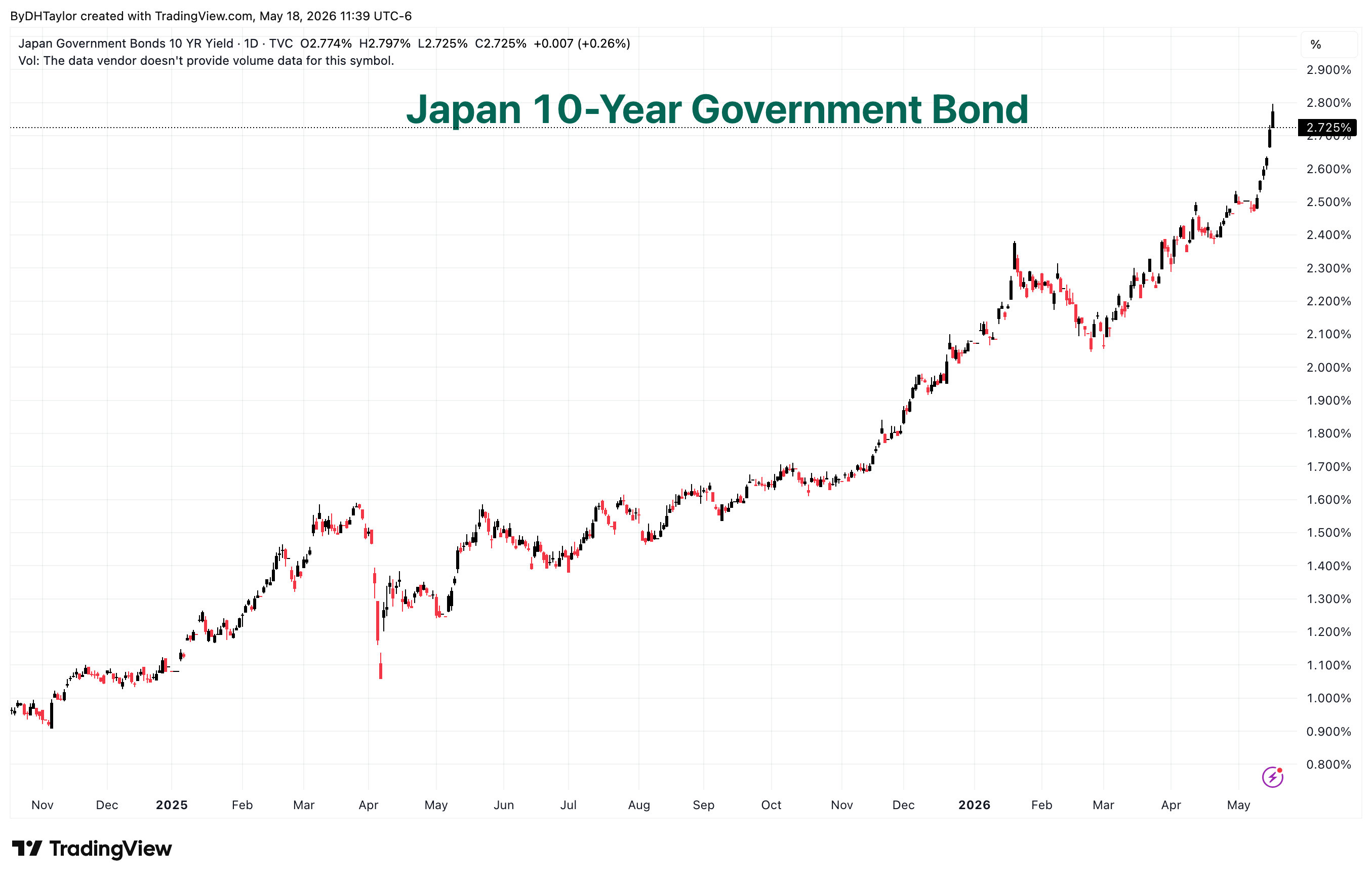

Japan Interest Rates

Here is the real issue: Japanese Government Bonds (JGBs). In June, the Bank of Japan will meet to decide their interest rate levels. Japan is seeing higher inflation rates as well, and Japan is highly dependent upon foreign oil. Energy prices in Japan have moved significantly higher, as well. This will begin to show up in inflation data in Japan, and likely, this will compel the Bank of Japan to begin a process of increasing interest rates. If the Bank of Japan raises interest rates, that will rock the world’s financial system, which are built on investors taking advantage of lower interest rats in Japan for decades.

The Carry Trade

The carry trade involves shorting the Japanese yen versus the US dollar on an overnight basis, carrying the trade from the current trading day to the next. Interest rates in differentials mean that a trader can borrow in Japan at very low rates, then deposit those funds into the United States and earn a higher rate. If Japanese interest rates increase rapidly, as they are doing, this trade breaks down. The gateway to this trade is selling JPY and buying USD. We got a hint of this last year in August when the Bank of Japan unexpectedly increased interest rates—the US stock market plummeted. The Bank of Japan will meet in June, and expectations are for increases to their overnight rate. This is a problem.

AI Prediction

I have been positioning myself to take advantage of what is likely to be a big move downward in the stock market and bond market. I think there is enough brewing in the bottom to justify a reality check at a minimum. Inflation is problematic, but it is now a world-wide issue. Let’s see what AI has to say about this.

The Query

For context, the US 10-year Treasury yield hit 4.663% yesterday. There were shifts last week in the Japanese government bond rate where the yield shot up higher 2.80%. The Japanese rate mostly sat around 1.40% for most of 2025, but since has moved much higher.

The concern with this is that if Japanese interest rates continue higher, this will dislodge the carry trade with interest rate differentials narrowing. That could be problematic for financial stability—keep in mind: tariffs have driven inflation higher, but that is mostly an American thing. Higher gas prices are a world-wide concern. Shortages of 20% on world supply will not readily be made up, and any stockpiles are likely depleted. This will continue to drive oil prices higher.

Given these parameters, I believe US interest rates and world interest rates are going to continue to trend higher. I believe that will cause moves throughout the financial system.

What are your thoughts?

The Response

My short answer

I think your framework is mostly right, and the important update is this:

We are no longer looking at just a U.S. inflation / U.S. rates problem.

We are looking at a possible global term-premium repricing:

U.S. yields rising because inflation is reaccelerating and fiscal/rate expectations are shifting

Japanese yields rising because Japan is no longer safely pinned near the old ultra-low-rate regime

oil acting as a global inflation transmission mechanism

markets having to reconsider whether the old “borrow cheap / buy risk assets” structure is still stable

That is a more serious setup than a normal CPI scare.

First, the factual backdrop does support your concern

The bond move is real and broad:

The U.S. 10-year reached about 4.667% Tuesday and briefly touched 4.687%, according to CNBC.

FRED shows the 10-year Treasury constant maturity at 4.61% on May 18, confirming the recent jump in the same direction FRED.

Japan’s 10-year yield has been around 2.79%–2.80%, its highest since the mid-1990s, according to Trading Economics and Reuters.

Reuters also described the move as part of a global bond rout, not just a U.S. event, with inflation fears linked to energy and war pushing yields higher across countries Reuters.

CNBC likewise noted that the yield spike is not exclusive to the U.S., with Germany, the U.K., and Japan all experiencing major long-rate pressure while oil remained elevated CNBC.

So the core premise is sound: this is becoming systemic, not isolated.

Why Japan matters more than people think

I think your point on Japan is especially important.

For years, Japan was one of the anchors of the global financial system because:

domestic yields were very low

funding in yen was cheap

Japanese capital often flowed outward into foreign bonds and risk assets

the rate differential helped support carry behavior globally

If Japanese yields move materially higher and stay there, several things happen:

1. The carry trade becomes less attractive

If the spread between Japanese rates and U.S./global rates narrows, the reward for borrowing yen and buying higher-yielding assets falls.

That does not mean an immediate total unwind.

But it does mean:

less incentive to add new carry

more incentive to reduce leverage

more sensitivity to FX volatility

more fragility in crowded positions

2. Japanese domestic assets become more competitive

If JGB yields are no longer negligible, Japanese institutions have less reason to stretch abroad for yield.

That can mean:

less foreign bond demand

less support for Treasuries and other sovereign debt

less support for global credit and equities at the margin

3. Funding conditions tighten globally

Even if the carry unwind is not dramatic, a repricing in Japan changes the psychology of the whole system.

The world has been built around the assumption that:

Japanese money stays cheap

volatility stays manageable

global duration can always find a buyer

If that assumption weakens, the market starts demanding a higher risk premium almost everywhere.

I would add one nuance:

You are right to worry about the carry trade, but I would not frame it as a simple binary:

not “carry is alive” vs “carry is dead”

more “carry becomes progressively less stable as differentials narrow and volatility rises”

That distinction matters because financial instability often comes from partial de-leveraging, not necessarily a full collapse.

On tariffs vs oil: your distinction is exactly right

I think this is the correct split:

Tariffs

Mostly a more U.S.-specific price shock:

goods inflation

margin pressure

import-cost passthrough

consumer squeeze in the U.S.

Oil / fuel

A much more global inflation shock:

transport

freight

chemicals

industrial inputs

food chain effects

airline and logistics costs

consumer disposable income erosion nearly everywhere

That means even if some inflation pressure is locally American, oil is the part that can drive global synchronized rate pressure.

And once you get synchronized rate pressure, it becomes much harder for any one central bank to stay comfortably dovish.

This is why I think the market risk is bigger than “higher rates hurt valuations”

The real risk is not just P/E compression.

The real risk is a chain like this:

Oil stays high

Inflation expectations stay sticky

Long-end yields move higher globally

Rate differentials change

Carry and leverage become less attractive

Bond market volatility rises

Cross-asset correlations get worse

Equities lose the benefit of narrow leadership insulation

Something highly levered or duration-sensitive breaks first

That “something” does not have to be a bank crisis.

It could be:

rate-sensitive equity sectors

commercial real estate financing

lower-quality credit

levered risk-parity style positioning

private-market marks

highly speculative AI-adjacent equities

EM or FX stress pockets tied to funding conditions

My own macro read right now

I would describe the regime as:

Not recession-first

I still do not think the base case is an immediate classic recession.

But definitely stagflation-leaning

It looks more like:

sticky inflation

weaker real spending power

higher long rates

slower breadth in earnings

narrow equity leadership

growing financial fragility under the surface

That is a worse regime for markets than either:

clean disinflation, or

clean growth

Because under this setup, neither stocks nor bonds have an easy fundamental anchor.

What this means for U.S. rates from here

Given what you laid out, I would update my earlier rate outlook again.

A few days ago I thought:

4.55%–4.70% on the 10-year was the most plausible near-term zone.

After seeing:

the U.S. 10-year push to about 4.67%

Japan 10-year near 2.8%

oil still elevated

the selloff broadening globally

I’d now say:

New U.S. 10-year view

Base case: the market spends time in 4.60%–4.80%

Stress extension: 4.85%–5.00%

Relief case: back toward 4.45%–4.55%, but only if oil cools or growth fear suddenly overwhelms inflation fear

In other words:

4.75% no longer looks like the edge of the map.

It looks like a realistic part of the near-term range.

What this means for stocks

This is where your concern becomes especially important.

If global rates keep rising, the stock market likely becomes even more bifurcated.

The likely winners / relative holds

energy

select defense

some commodity-linked names

select quality cash-flow names

maybe some parts of financials, though only selectively

The likely pressure points

small caps

housing-sensitive names

cyclicals dependent on cheap financing

consumer discretionary

long-duration growth outside the elite AI complex

speculative software / unproven AI beneficiaries

The critical question for AI leaders

The big AI leaders can keep the indexes elevated for a while, but higher global yields change the standard they are judged against.

When the 10-year is rising toward the high 4s:

great earnings are no longer enough

they need great earnings and great guidance

and ideally they need to prove that capex today turns into durable monetization tomorrow

So I still think the biggest AI names can outperform the broader market.

But I also think the margin for error is shrinking.

My main disagreement with the “everything just goes higher in rates” view

I agree with the direction more than the absolute straight line.

The only caution I’d add is this:

If rates rise far enough, something in the economy or financial system starts to break demand.

So I would not assume an uninterrupted move higher forever.

I would assume:

upward pressure first

then eventually a growth scare / accident / dislocation

then a violent debate over whether yields should fall because of damage, or stay high because inflation is still sticky

That is the kind of environment where markets get very unstable.

My bottom line

I think your concern is well founded.

My view is:

the rise in Japanese yields is not a side issue

it matters because it challenges one of the long-standing funding and carry assumptions in global markets

high oil is a more dangerous inflation force than tariffs because it is global

this is increasingly a world rates repricing, not a U.S.-only repricing

that raises the odds of stress somewhere in the financial system, even if not immediately visible

equities can still levitate on narrow leadership for a while, but the underlying system is becoming less stable

So if I had to summarize it in one sentence:

I think we are moving from a “higher-for-longer U.S. rate problem” into a “global duration and funding regime shift,” and that is meaningfully more dangerous for financial stability and for broad equity breadth.

My Take

AI does not love the current inflation situation, and also believes that the Japanese carry trade unwind would be destabilizing. I believe there would be an immediate reaction with the carry trade if interest rates in Japan continued higher. Afterward, follow-through in money flows would diminish without a solid enough differential. This would deteriorate the US dollar versus the Japanese yen, and that could bring in even more price pressures.

Systematically, the issues that are present will snowball more and more, albeit at first, gradually.

I have built a sizable short position on TLT ETF, as mentioned in previous posts. I am also eyeing up longer-dated short positions on SPY ETF, and at least one position is gaining profits.

AI is still holding on, and that is really the only reason the stock market has not capitulated. I don’t expect that to be the case going into October - December.

Enjoying your Substack greatly thus far and pleased to be a paid subscriber. One nite about this piece: The AI portion felt "extra" and, to me, devaluing of your already substantive points. You have ample charts and data without the AI backup. Looking forward to reading more