Don't Believe the Employment Data

Headline numbers show steady unemployment numbers, but the headlines need a deeper dive to see the true story

On Friday, we got the non-farm payroll data and the unemployment data for the month of April. Unemployment held steady, but there are issues with the data that if you do just a simple dive into, you can see that the current number is a bit misleading.

Look at the chart above: There is a noticeable decline in the Civilian Labor Force, and the number of Employed Civilians. While one or two months showing some moves is interesting, this is now four months where there appears to be some peek in the Civilian Labor Force and those employed. This has brought down the total number of employed, but the unemployment rate remains steady—this is misleading to me:

Keep in mind, the unemployment rate is a percentage. If the total number of the labor force declines, and there is an in-kind decline in those employed, the unemployment rate may hold steady, and the stock market could take that as a positive.

I had a very lengthy conversation with AI on this to reiterate some of my working assumptions. AI believes that there is skew here, and that evidence exists that there is some dropping off because of discouragement in finding a job—some individuals want jobs, but stopped searching because they are not getting anywhere. This may be what is pulling down the Labor Force numbers, and this that are employed within that.

I have never really been a bit fan of the non-farm payroll numbers. This number is dependent upon a survey, and the data can be iffy at times. The market always makes a big deal about the increase / decrease. Yet, the numbers can be misleading.

It is difficult to get a real read on what could be next with non-farm payroll gains or losses. The numbers are down significantly from previous levels. There was such a strong surge in rehiring after the COVID shutdown, and continuous trickle downward from that point forward, you have to wonder who’s left to be brought onto payrolls? The answer to that is simple: The disgruntled job seekers.

There is something else to consider: The really, really big picture of employment opportunities over the past 35 years.

Make America the 1900s Again

This chart above is a 12-month rolling sum of all jobs added—or, lost. Something jumps out at you if you are looking: The 1990s saw the biggest overall gains collectively, relative to all other periods. Keep one thing in mind when you consider that: This number is a real number, non-adjusted. The population was far lower in the 1990s than it is currently. Yet, on a hole basis, more individuals were collectively brought onto payrolls than more recently. On a percentage basis, versus the population, the biggest surge in employment occurred in the 1990s, versus any other period.

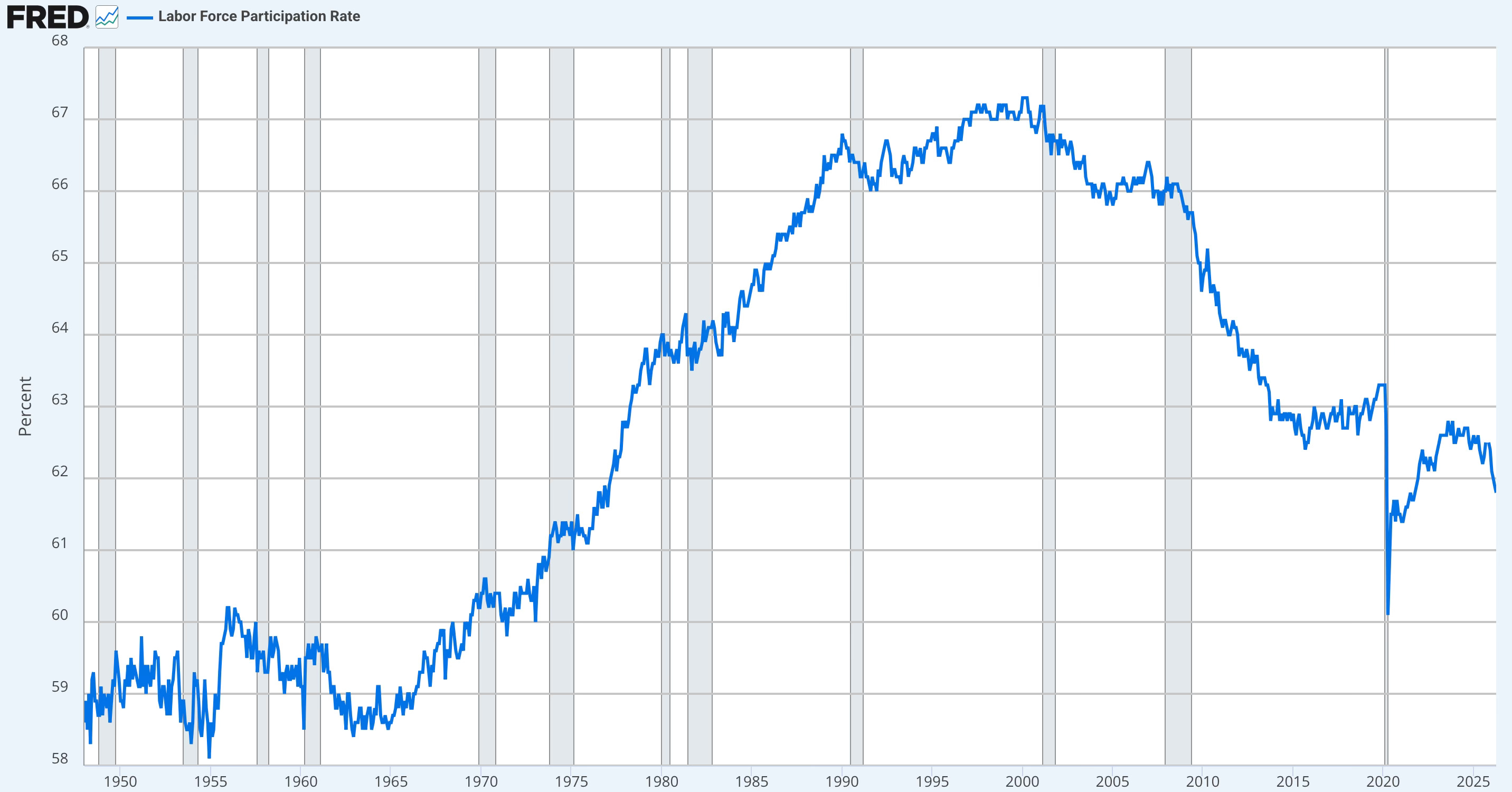

Women do not account for this as they entered the workforce, as that big surge started in the 1960s through to the 1980s. Also, the participation rate held steady through the 1990s, shifting all of 1%:

The above participation rate chart shows how individuals are simply leaving the workforce as the country reverts back to earlier levels.

In the meantime, what to make of the current employment levels?

Interest Rates

I have entered into new positions shorting Treasuries (prior to the inflation data release on Tuesday morning). Employment numbers will not force the Fed to make any quick decisions, but instead, give the Board enough ammunition to focus on other issues.

I believe that the inflation story is just getting started, and that higher oil prices are now a permanent feature. Higher oil prices will eventually trickle through the entire economy as the economy absorbs the oil shock and attached price increase.

Since employment has largely not been affected from the tariffs, this gives the Fed room to address the persistent price increases. I believe that US Treasury interest rates will continue to move higher. Because of this, I have taken a short position on TLT ETF via buying puts.

More on that below.

Equity Markets

Another aspect I have been asking AI about is the continuous rise in the AI trade, and a few other stocks.

There are the usual five stocks that are leading the AI trade. There are a few others now that are also driving the stock market. According to AI, there are some 12 others that are a big reason the stock market has surged. That means there are some 17 stocks that are largely the reason for the big surge up from 630 to 740 in SPY ETF.

The rest of the 483 stocks are not moving much at all, and if the economy breaks, these 483 may pull the rest of the stock market down.

Then… if AI breaks and falls short, the downward move in the stock market may rival that from the financial crisis.

AI Prediction

As I mentioned, I have begun building up a short position in TLT ETF. I am using vertical put spreads having put the initial position on Monday morning. I felt the inflation data would be hotter than expected, and that is what happened.

For some time, I have been sitting on the Treasury inverse ETF, and that has gone higher. Over the past year, I have been selling TLT ETF vertical call spreads to collect premium, and that also played out over time. Now, I will sit on the current positions and get ready to add into them.

The Query

Okay… let’s consider what may happen in the stock market over the next few weeks. First, the US 10 year treasury yield has risen to 4.48% today. This is being driven by a few things such as the surge in the CPI data we got on Tuesday, and what most believe will happen further with the high price of fuel. I believe that gas prices being high are a permanent feature because I do not believe that Iran will budge, nor that the US has any real negotiating position in this.

I had asked you previously about the US 10 year, and you felt the current regime would support the potential of the yield to increase to between 4.50% and 4.75%. the landscape has changed, and I am wondering if you would like to update that outlook?

Next, another question I had for you was the list of stocks that are driving the market now. There is, of course, the big five that are really pushing things, and you listed an additional 12 more that are fueling the move. While there is real earnings being driven for these stocks to continue higher, I first want to point out that the other 483 stocks could turn downward if the economy does.

How much of the current earnings are priced into these Ai stocks, and is the consensus that they are overbought, r are valuations about appropriate?

The Response

Short answer

Yes — I would update the 10-year view.

A few weeks ago, 4.50%–4.75% looked like a reasonable upper testing zone. With the 10-year now around 4.48%, a hotter CPI, hot PPI, firmer oil, and the market sharply reducing cut odds, I’d say:

• 4.50% is no longer the “test” level — it is basically the doorstep

• the center of gravity has shifted upward

• the market now looks more biased toward the upper half of that old range than the lower half

My updated view for the next few weeks would be:

• base case: 4.55%–4.70%

• stress case / overshoot: 4.75%–4.85%

• less likely bullish-bond case: retreat back toward 4.35%–4.40%

That is a more hawkish view than before.

Why I’d update it upward

The new information matters:

• Tuesday’s CPI came in hot, with annual CPI at 3.8%, above expectations, and core also above expectations according to CNBC.

• Today’s PPI was even worse for rates, with headline PPI +1.4% m/m and core +1.0% m/m, which pushed the 10-year to 4.48% and reinforced the “higher for longer / maybe even tighter” message according to Schwab.

• Oil is still elevated, with Schwab showing WTI above $102, and the market is clearly treating energy not as a one-off blip but as something that can bleed into broader prices and margins Schwab.

• The bond market has also been hit by weak demand at auction and by the market pushing out rate cuts; Schwab notes futures now show only a very small chance of cuts this year and materially higher odds of hikes than before Schwab.

So the story is no longer just “sticky inflation.”

It is becoming:

1. headline inflation is re-accelerating

2. pipeline inflation is re-accelerating

3. energy may persist

4. the Fed is boxed in

5. long-end yields are doing more of the tightening

That is a more hostile rate backdrop for equities than the one we were discussing earlier.

Where I think you are right

I think your point about fuel being a persistent feature, not a short-lived spike, is the most important change.

If oil remains elevated because the geopolitical situation does not resolve, then the market has to think about:

• transportation costs

• input costs

• household cash-flow squeeze

• inflation expectations

• reduced room for Fed easing

• a higher term premium in long rates

That combination is exactly what pushes the 10-year from “upper range test” into “regime repricing.”

My current rate view

So if I update my prior outlook honestly:

Old view

• likely test of 4.50%

• difficult to sustain much beyond 4.75%

Updated view

• 4.50% is now very likely

• 4.60%–4.70% looks increasingly plausible

• 4.75% is no longer a stretch scenario

• a brief spike above 4.75% is now more believable than it was before

What I’m still not ready to say is that yields will just run away much beyond that and stay there.

Why not?

Because once you start getting into the high 4s, financial conditions begin to bite harder:

• housing affordability worsens

• credit stress rises

• multiple compression intensifies

• cyclicals get hit

• weaker breadth becomes more obvious

• the market eventually starts pricing slower growth damage

So I would say the new regime is higher, but not endlessly higher.

Now to your second question: AI stock earnings and valuation

Here’s my cleanest answer:

A lot of the near-term earnings power is already priced in

But not all of it — and not equally.

That is the important distinction.

The market is not pricing these names as if they are frauds or empty stories. The earnings are real. But it is also not waiting around to discover that anymore. It has already capitalized a large amount of:

• AI infrastructure demand

• hyperscaler capex

• continued accelerator demand

• cloud monetization

• margin durability

• multi-year EPS growth

That means the issue is no longer:

“Are the earnings real?”

The issue is:

“How many years of exceptional earnings are already embedded?”

And I think the answer is: quite a lot.

My view of the valuation setup

I would break the AI leaders into three buckets.

1. The top-tier AI infrastructure names

These are the names where the earnings are strongest and most visible.

For this group, I would say:

• valuations are rich

• but not necessarily irrational

• and in some cases, they’ve actually compressed relative to growth

For example, the broader “Magnificent 7” forward P/E has compressed to around 24x, while some of the group trade closer to high-teens to mid-20s forward multiples, according to MarketBeat. Nvidia specifically has been discussed as trading around the low-20s forward earnings in some recent analyses, even after its huge run, while analysts remain split between “fairly valued” and “limited upside because so much is already priced in” Yahoo Finance.

So for the very best names, I would not say:

• “obviously absurd bubble”

I would say:

• “expensive, but supported by extraordinary earnings momentum”

2. The second-line AI beneficiaries

These are companies benefiting from AI enthusiasm, but with less certainty around monetization or durability.

Here the risk is much higher that:

• the multiple expanded faster than earnings quality improved

• future demand is being extrapolated too generously

• the market is paying for AI optionality that may not fully monetize

This is where I think “overbought” becomes a more reasonable label.

3. The AI-adjacent speculation layer

This is where “AI” acts more like a thematic premium than a proven earnings engine.

For these, I think:

• yes, many are overbought

• and if macro worsens, they could derate fast

What consensus seems to be now

The consensus, from what I’m seeing, is not “AI stocks are universally insane.”

It is more like:

• earnings are genuinely strong

• valuations have already absorbed a lot of that strength

• the biggest leaders have had some multiple normalization rather than pure blowoff expansion

• but the market is increasingly vulnerable because upside now requires continued execution, not just the story

That lines up with recent commentary that broader U.S. tech valuations are no longer at the extreme premium they were previously, with some strategists arguing that strong earnings have made parts of the group look more reasonable again CNBC, while others still warn that much of the upside is already in the price and that the downside is underappreciated if capex or monetization disappoints Yahoo Finance, Reuters.

My own interpretation: what is priced in?

I’d phrase it this way:

For the top AI names, the market has probably priced in:

• most of 2026 consensus

• a meaningful chunk of 2027 optimism

• continued high capex

• continued AI demand leadership

• continued margin support

So if you ask me whether these stocks are priced for:

• “good earnings” — yes

• “very good earnings” — mostly yes

• “excellent earnings plus raised forward guidance” — that is where the upside still lives

• “any stumble at all” — not well tolerated

That is why I would say they are not cheap, even if some are not historically outrageous on forward P/E.

Your point about the other 483 stocks is the real structural risk

I think this is the most important part of your question.

If the economy weakens, then yes, the other 483 stocks can absolutely roll over even while the AI leaders continue to post strong numbers.

That creates a market where:

• the index headline can stay deceptively strong

• breadth deteriorates

• cyclicals and small caps weaken

• equal-weight underperforms

• economically sensitive earnings estimates start getting cut

• the market becomes more fragile beneath the surface

In that setup, the AI winners can keep the major averages elevated for a while, but they cannot fully immunize the market from macro deterioration forever.

Eventually one of two things happens:

1. the AI leaders keep accelerating so hard that they offset broad weakness for longer than expected, or

2. the market starts questioning whether even these leaders deserve their premium in a weaker economy and higher-rate world

That second step is the real danger.

My bottom line

On the 10-year

I would update my view higher.

• Previous range: 4.50%–4.75%

• Updated bias: more likely to live in 4.55%–4.70%

• 4.75%+ is now more plausible than before

• sustained move much beyond that is possible, but I’d still view it as more of a stress extension than the base case

On AI valuations

I would say:

• the earnings are real

• a lot of the near-term earnings are already priced in

• top-tier AI leaders are expensive but not automatically absurd

• second-tier / AI-adjacent names are much more vulnerable to being overbought

• if the economy rolls over, the other 483 can absolutely weaken even if the AI complex initially holds up

So my best one-line answer is:

The top AI stocks are not universally “too expensive to own,” but they are increasingly priced for continued near-perfection in a macro environment that is getting less forgiving.

My Take

On some level, the AI stocks rightfully are pushing the stock market higher. On another level, the bottom tier Ai stocks could fall easily if they do not perform. The other stocks in the stock market are likely to wobble hard, and that is what I believe will be occurring soon. The future of interest rates will be higher, and that will be restrictive for the economy.

I have been entering bigger short-term positions on TLT ETF with the idea that given the current information, if the US 10-year Treasury yield hits 4.65%, I take profits and likely flip. That depends upon what would occur next with oil and the tariffs.

I want to know more about the second & third tier AI stocks going into the future—I think that is crucial.