Google Sold Its Stock At The Top... Did You?

Google sold some $80B of its own stock, which may be a tell of where the AI craze is. It may also be time to reevaluate.

Alphabet, the parent company of Google, raised capital for its AI buildouts to the tune of $85B using equity financing, and this caught the market off guard. Originally for its buildouts, they were relying on cash flow from operations. When that well dried, they took on debt—as well as many other players in the arena. Now? Equity offerings.

What makes this most surprising is that throughout the past decade Alphabet had actively purchased its own stock to boost shareholder value. All of a sudden, they flipped a U-turn.

My first question was: If Alphabet was actively buying back stock to boost value, wouldn’t offering out stock dilute value?

CFOs will use equity financing as a method of last resort—equity offering is the most expensive way to obtain capital for a company.

Or is it?

In the case of the Alphabet offer, maybe the CFO sees the valuation so rich that not selling shares would be an expensive way to raise capital despite diluting shareholders.

Either way, both point to GOOG stock heading lower and this cannot be ignored.

A Bad Week For Equities

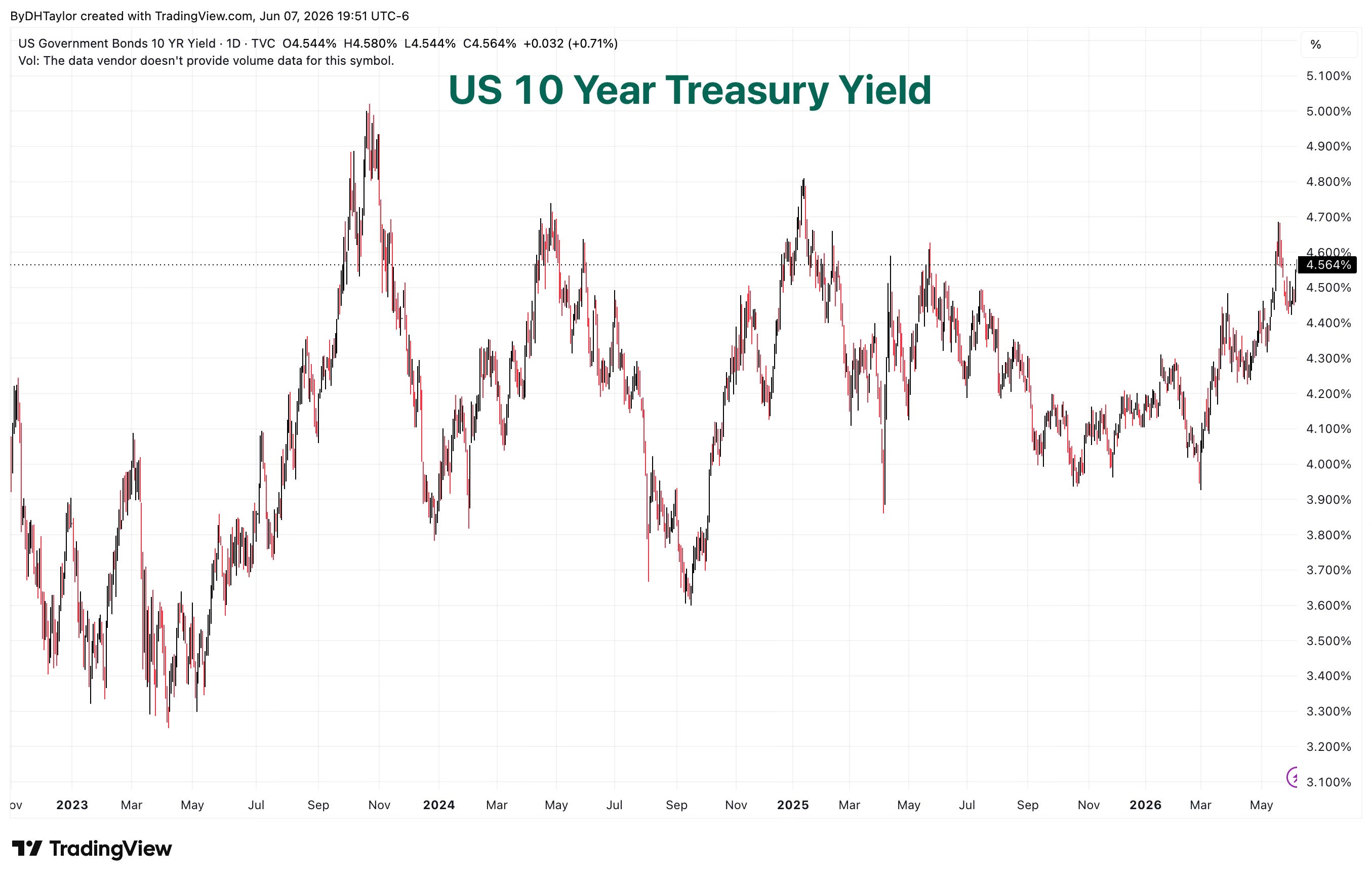

In the meantime, last week saw the Nasdaq take it on the chin. US jobs data printed such a big number that traders are now looking at the potential for the Fed to either leave interest rates where they are for far longer, or even hike rates—I have been calling for higher interest rates since September 2024 when the Fed actually cut rates just before the Presidential election.

My belief is that Friday was more than just a bad day for Wall Street—here are the bullet points I am looking at:

Rates will stay higher for longer or go up

Economic growth is slowing and I’ve covered multiple charts lately that substantiate that from many angles

Capital is getting more expensive

Expectations for AI revenue are enormous

The AI buildout may be outrunning the near-term cash flow

I believe these represent a solid working thesis, and I have been covering pieces of this in recent posts.

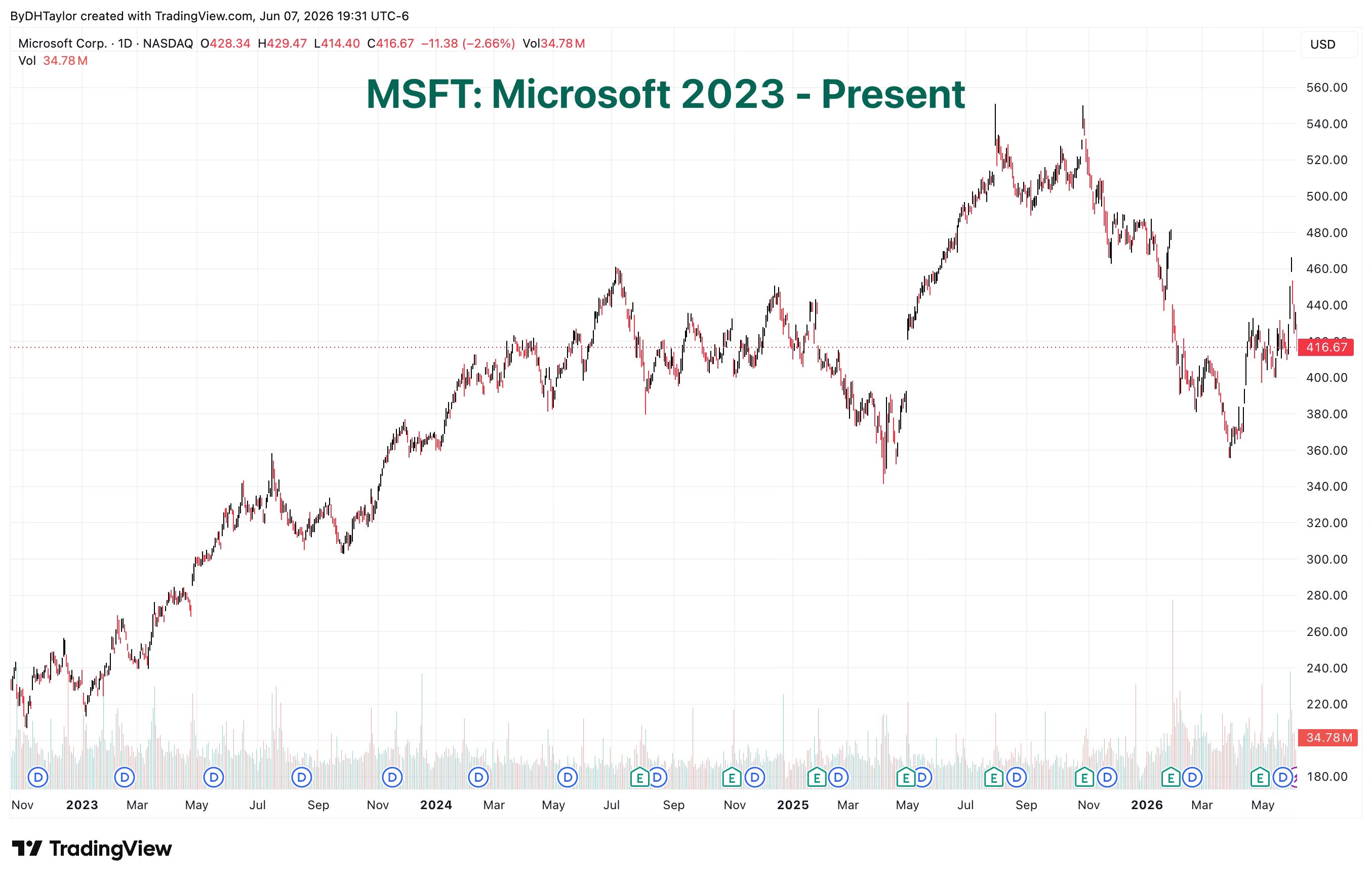

There’s more to the move lower on Friday with Broadcom and Microsoft making some waves, and this makes the Alphabet story more compelling.

A Bigger Backdrop

It is not just Alphabet’s equity offering that is important to note, nor what I am keeping track of. In multiple posts, I have outlined the economy and how growth is slowly dragging lower and lower—I am not calling for a recession, but growth rates are narrowing.

Beyond simply the broader economy, other players in the AI world had bad days, or are showing signs that there may not be a clear path to profits.

Broadcom

Broadcom - AVGO - sold sharply after its latest earnings release. There is significant growth, and Broadcom is capturing that. The only problem is that the growth rate is no longer outlandishly hyper-fast, but merely really, really hot. That’s not good enough, and AVGO stock to get offered.

Microsoft

A leaked internal memo from Microsoft said that they are pulling back on usage of AI, and are opting to use humans instead. The reason? Cost—it is cheaper to have a human do the tasks than to have AI do tasks.

Keep in mind the relationship that Microsoft has with OpenAI in that they are heavily invested… and yet the math of using AI is not mathing.

This calls into question the potential payout for AI if one of the biggest players and investors in AI says it is not cost effective—what about the rest of America?

This is subject angle that I have touched a couple of times in that I simply don’t see where the measurable profits will come from if the costs are so great. Microsoft is reiterating this with the leaked memo. Traders may begin reassessing realism. Profit taking may begin.

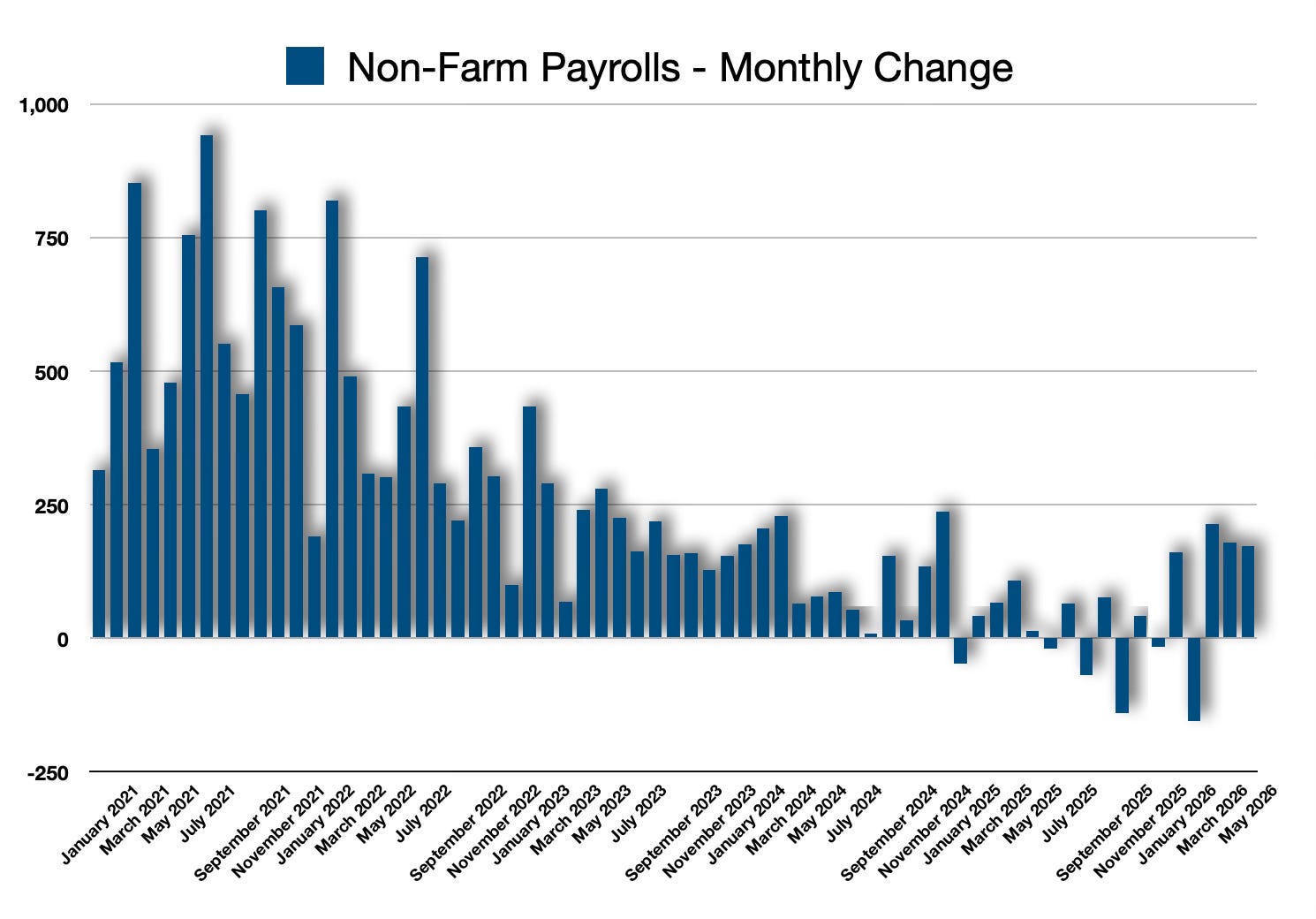

Employment

The latest jobs data printed revised numbers higher for previous months, as well as well-above expectations print for the month of May. This print sent bond yields much higher with the expectation that the Fed now has all the slack necessary to raise interest rates in order to regain control over sticky inflation. Prior to the launch of the war with Iran, inflation had been trending back upwards. Now, there is more fuel to add to the reasons why price pressures will increase.

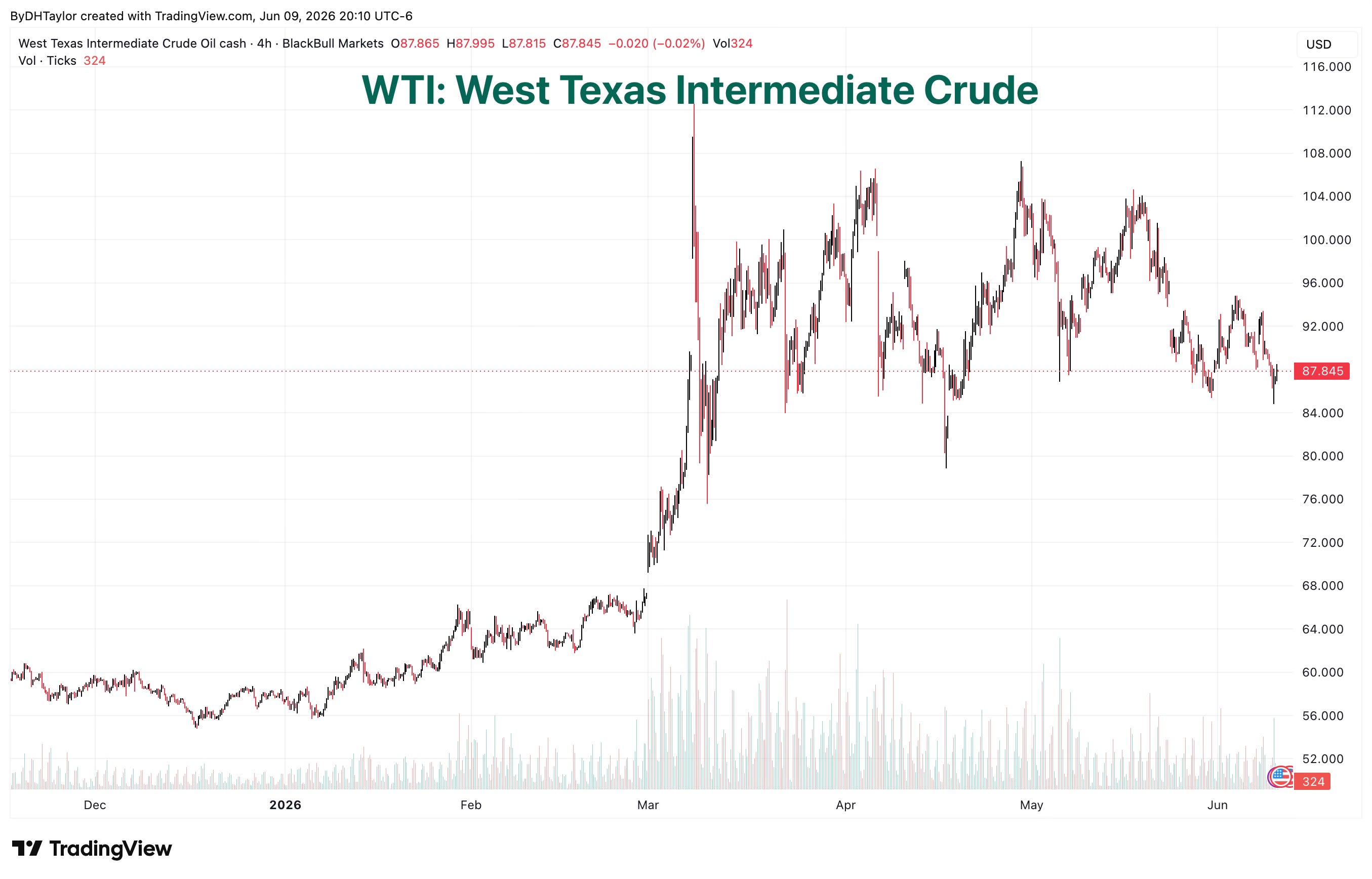

The one thing to note about inflation is that with the tariffs, price increases were felt almost entirely inside the United States. With oil price increases, this will be a worldwide phenomenon. That will add even more fuel to the fire.

My Take

It isn’t just one thing, it is many things. All of the little things are adding up to something bigger, and a regime shift in interest rates, along with greater scrutiny for AI stocks may be starting, and that could weigh on the overall market.

Interest Rates

Interest rates are going higher. The increase in price for oil is far from over, and this is going to be felt globally.

While this is one angle of what is happening with the economy, there are multiple pieces—it’s never just one thing.

When you factor in what Alphabet did, when you look at other players in the AI realm, and then you also encompass oil and the economy, it’s easy to see that many pieces of the puzzle are adding up to a shifting potential.

Oil

My base-case is that while Trump may have thought that Iran would simply crumble with the first attack, there’s something else likely occurring. His son-in-law is heavily invested in the oil industry, and likely just made a killing with the rapid rise in price. Given that, keeping the Strait closed would be in line with all of the other gambling going on in the White House. While the oil market has priced in a resolution, I don’t believe there will be one for many months, if not a couple of years—after all, there’s trading profits to be made.

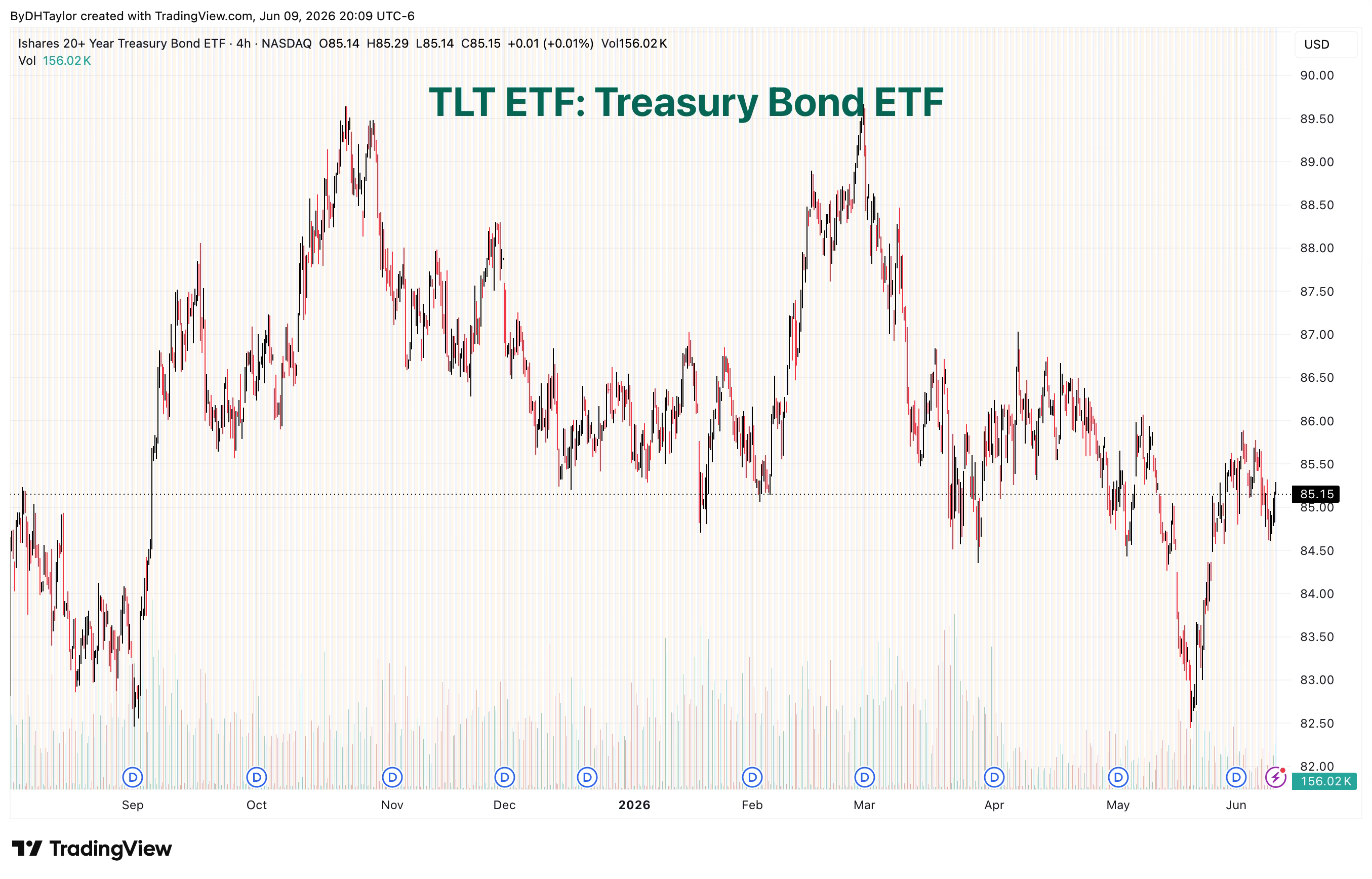

TLT ETF

I have been short Treasuries for some time in one manner or another. My most recent additions were buying puts on TLT ETF, and the latest moves in the markets have added to some profits—I am targeting sub-$80.00 for my first take-profit on this trade. Price pressures were already increasing prior to the launch of the war with Iran. Now that oil prices are significantly elevated, there will be more price pressures. The answer to that is higher interest rates.

Given that, and considering the slack the Federal Reserve now has because of solid employment, I expect interest rates to continue a gradual move higher, possibly in a range of 4.75% - 5.00% for the 10-Year. That will put a real damper on the stock market… and that is making the CFO of Alphabet look even better—he likely sold at the top.

The AI Trade

There is compelling evidence that the AI trade may be nearing an end, and that this will no longer be a successful trade where you bet everything on an up move. Instead, considering the financials of the buildout for AI, investors may now be wary of all of the capital investments without some kind of return. The idea of circular investments being a wobbly foundation may start to merit real concern.

Adding in factors such as the broader economy with increased price pressures in a regime of increasing employment, higher interest rates may rattle the broader stock market.

I do not see a full-blown sell off in the AI trade, but the endless move higher may be harder to achieve. More scrutiny may show up as companies are stressed about raising capital. While I have participated in the AI trade on some level, I think we see a new regime, and this could pull stocks lower.