How AI Buildout & Tariffs Are The Cause Of Inflation - Not Oil—yet!

AI and tariffs are the real cause of inflation. Oil will add even more, and here is what to watch.

Inflation is running hot. Core PCE inflation, as measured on a year-over-year change, is well above the 3.00% level and trending higher. Most are focused on the here-and-now of the oil prices shooting up, however, price pressures were heading higher well before the February 28th launch of the Iran / US conflict.

While oil prices are going to add significantly to future inflation, currently there are two real causes of inflation being driven as of right now:

Tariffs

AI Buildout Demand

AI facilities are being built at an alarming pace, and demand for goods to build many of what is necessary for the components are significantly outpacing supply. Because of this, prices for raw materials have been increasing at a rapid rate.

It is not simply raw commodity prices that are moving rapidly higher, either. Also, prices for finished, intermediate goods, such as memory and processing units are also seeing price increases from outpaced demand.

Adding in to the price increases from AI demand are the costs of tariffs to both consumer goods and producer goods, which have pushed prices of items such as steel, aluminum, copper, autos, pharmaceuticals, as well as food and energy items. The brand increase has pushed these prices upwards some 3.1%, according to the Federal Reserve, and this has added about 0.8% to PPI inflation gains.

PPI Inflation

All of this will trickle into the broader economy. Producer Prices have also been trending higher because of the demands raw materials for the AI buildout and the increased costs from tariffs.

Inflation will be a part of the economic landscape for some time until the Federal Reserve slows overall aggregate demand until price pressures abate to growth rates that are aligned with balanced economic activity.

There are two caveats to this, however, and then an asterisk:

If the AI bubble bursts, and demand for the AI buildout declines, commodity price pressures would naturally trend lower

If Trump’s latest tariffs get struck down again, this would alleviate price increases

Employment: The Asterisk

Oddly, employment has been robust. while there have been many hurdles for the economy to jump through, various aspects of the economy have remained robust. There are strains, however, and one need look no further than the savings rate which is near its all-time low, delinquency rates for credit cards and overall credit levels, which have trended significantly higher.

On the one hand, this will give plenty of room for the Federal Reserve to increase rates in order to combat price pressures since its dual mandate is price stability and full employment.

On the other hand, I simply have a tough time with these data points and feel there will be a massive revision at some point in the future, negative all of the positive effects we believe we are enjoying.

Time will tell.

Oil

Mostly through 2023 - present, oil prices have not moved significantly that would contribute to inflation, notwithstanding the jump in February. Most of the increases in inflation over the past several months began prior to the conflict, and therefore we can eliminate oil as a cause.

That being said, because of the price of oil jumping as it did, there may be short-lived inflation coming, but I expect that to turn back around.

In the meantime, over the following few years, many countries will be acquiring oil diligently in order to increase their respective reserve levels.

Metals

Copper

While a conversation-like system was announced to the general public in November, 2022, and while many companies began an integration process, many hyper-scalers went CapEx-heavy in late 20223 - onward. You can see the scale occurring in 2024, then accelerating through to the present.

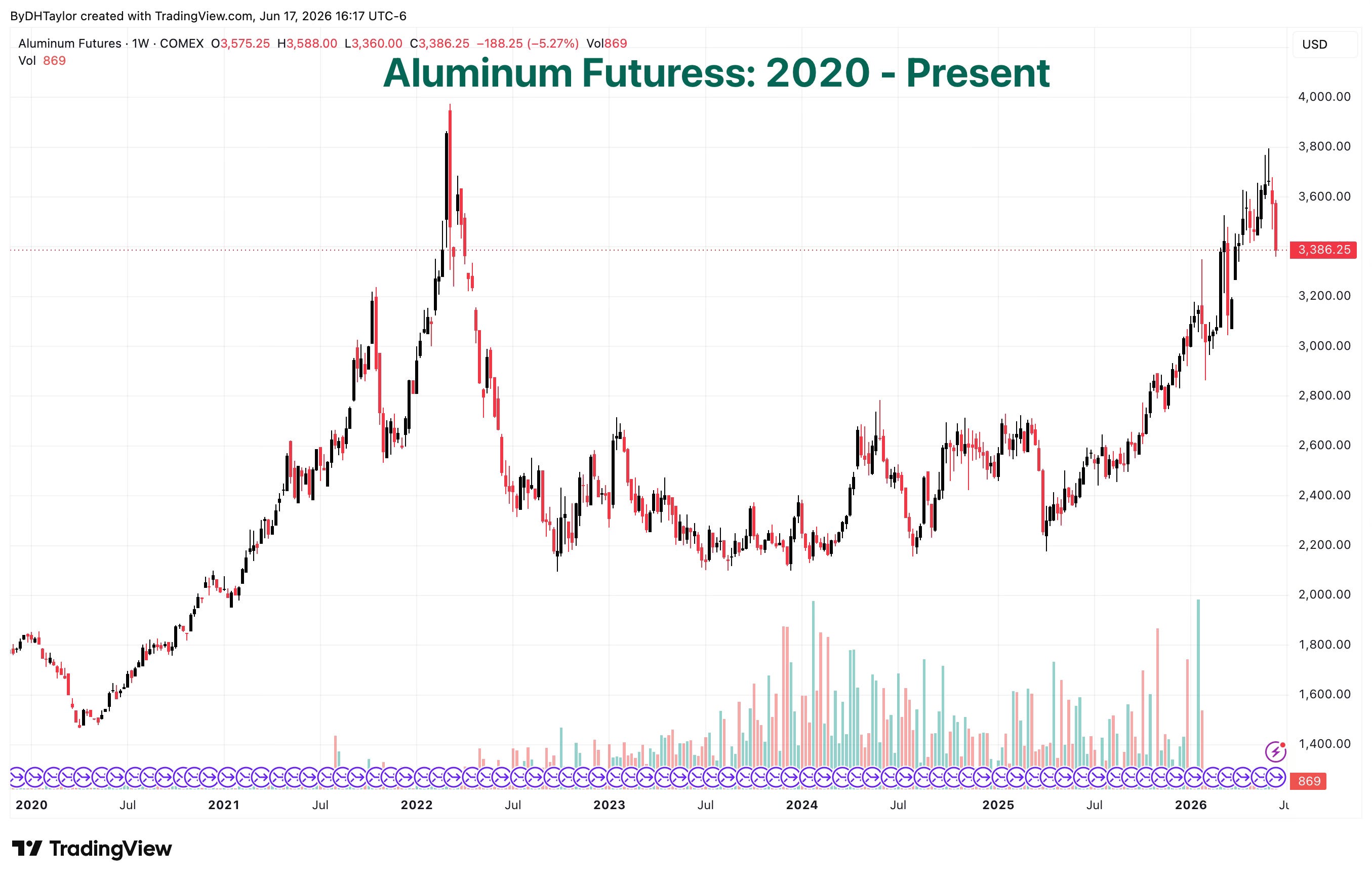

Aluminum

Aluminum futures have also gained during this time of hyper-CapEx building for AI facilities, along with the overall upward trend in imported metal prices since “Liberation Day”.

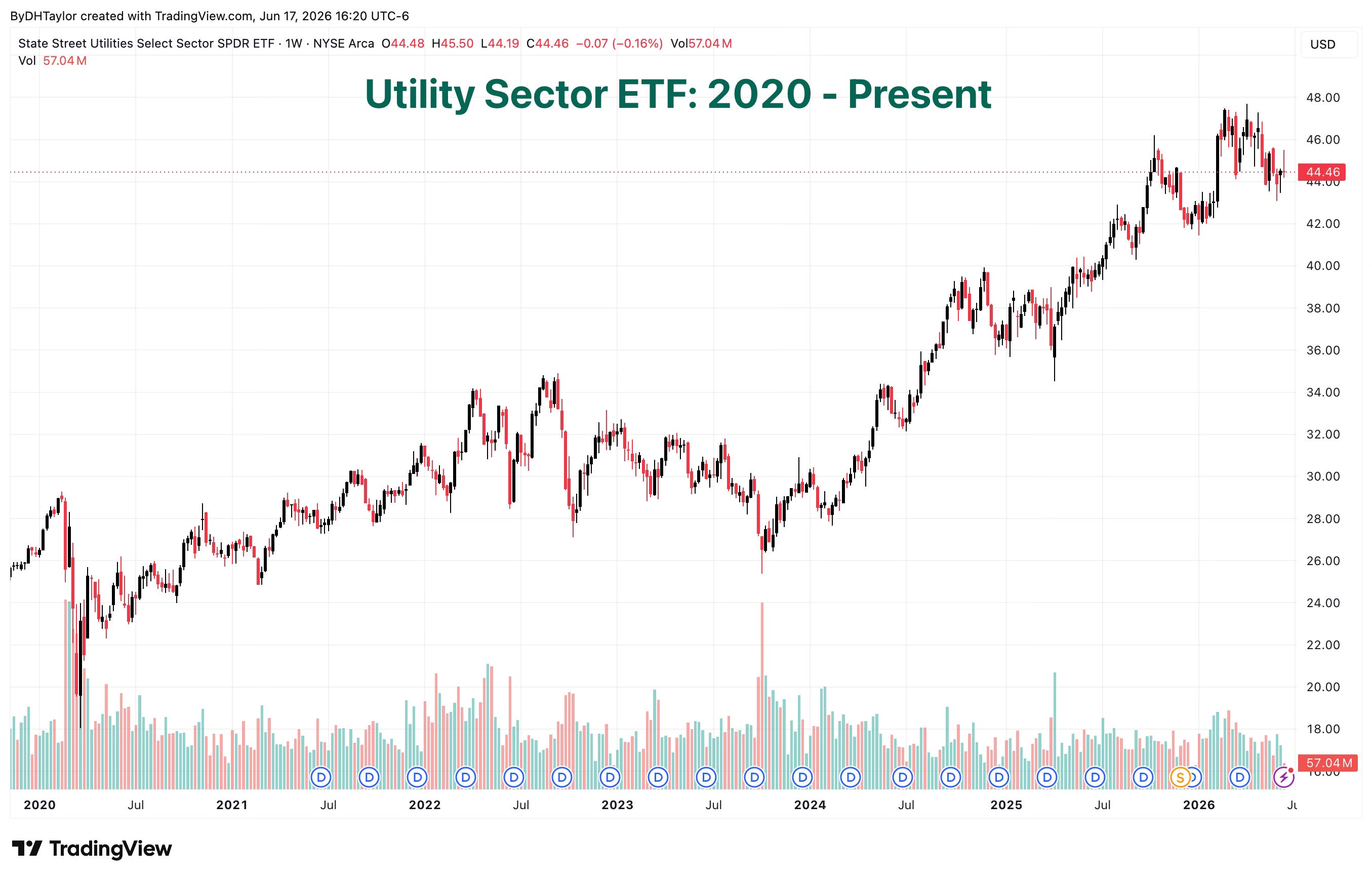

Utilities

Data centers need power… lots of power. The chart shows how much demand is affecting the sector price as demand outpaces supply for power, and energy sector stocks continue to gain more value.

I wonder, however, if there is a reality check with AI, and companies begin scaling back on buildouts, peer usage may drop as well, and ultimately utility stocks’ prices.

In the meantime, this could be a solid trade moving ahead until capabilities increase.

Interest Rates

For some time now, my position is that interest rates are going higher. In September, 2024, I believed that the Fed should not have lowered interest rates at that time because long-running inflation growth would not hit its 2.00% target level. It has not. I believed then that interest rates would have to remain higher for longer, or maybe even head back upward lest inflation begin trending back up. Inflation began trending higher since then, and I believe this warrants increasing interest rate levels for some time in order to bring inflation down to its target level.

There are caveats to this, of course, in that if the AI buildout begins to feel like a bust, all of a sudden there will be a fire sale of far too much AI equipment that will become obsolete faster than it can be sold. The stock market is beginning to feel nervous about AI, and recently there has been some selling–that could be a big problem.

Another caveat to this is that tariffs may be struck down again, and almost immediately, prices for goods and services would fall, and this would bring inflation down with it.

I actually believe both of these scenarios are likely to occur, and their effects would help considerably.

TLT ETF - My Position

In the meantime, I am still long puts on TLT ETF as I look for a solid move below the $80 level, however the market has remained flat-ish. If the market does not move below my target levels, having used a synthetic position with vertical spreads, I would still end up profitable, however with very small results.

My belief is that interest rates will go higher, and additional economic data points are going to reiterate this more and more as time moves forward.

I am still in a short SPY ETF position with targets sub 700.00, and that is beginning to turn profitable—I’m in positions all the way out to December.