Treasury Yields May Break Out—That Will Be Devastating

Price pressures are gaining, and $200 oil potential will only worsen the situation. If the 10-Year breaks out, the stock market could be devastated

My go-to indicator is the US Treasury yield on the 10 to determine how the market is functioning given any recent economic event, or as of late, geopolitical event. The US 10-Year Treasury yield looks as if it is potentially packing possibilities. Not much good is presenting itself economically that would perpetuate a growing economy. Instead, almost everything seen in the past month has looked worse than anticipated:

Price pressures are increasing

A new war that has the potential to push oil prices to $200.00 per barrel, potentially dragging on the economy further

Personal incomes & personal expenditures are declining, removing the engine of growth for the consumer-led economy

While there was an increase in CPI inflation in the last report, there has been a divergence with PCE that is printing a more dire outlook.

Given some of the economic indicators I have seen, I do not know how the stock market remains afloat. While there has been some downward pressure, I expect far more.

Personal Income & Personal Expenditures

The latest data—and revisions—brought the trajectory of both incomes and expenditures downward. In themselves, they are not necessarily telling, but add to a total story. Incomes and expenditures go hand-in-hand, and this makes a lot of sense. If the rate of growth in incomes increases on an annualized basis, you will see the same with expenditures. The correlation is not a perfect 1, but is highly correlated, of course.

The United States is mostly driven by the consumer, and so if there is a declining rate in incomes and expenditures, this will eventually show up on the top lines of the major corporations’ revenues. If there is a decline in the pace of revenue growth, the stock follows suit.

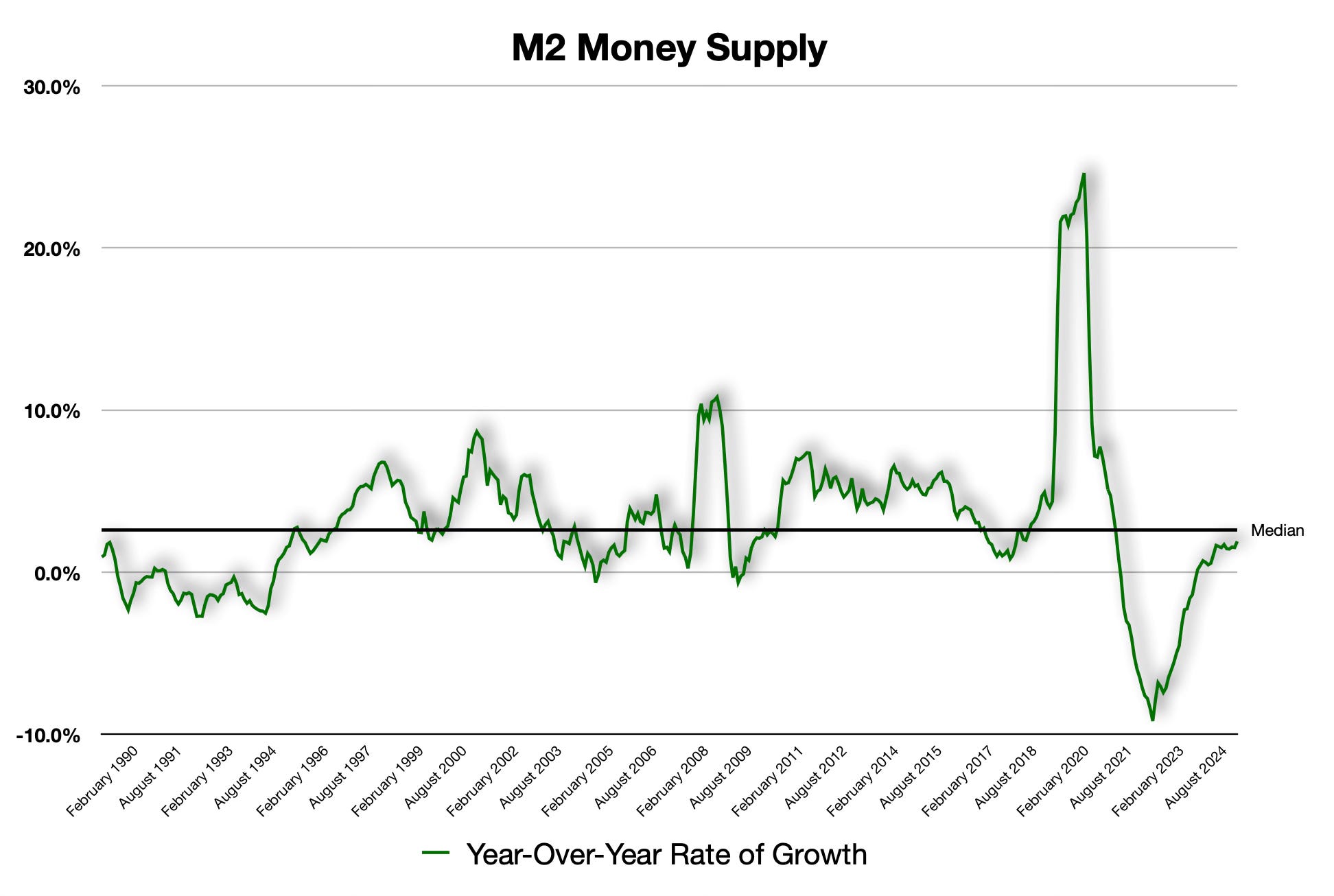

The money supply is the other real indicator that I follow to see what will happen next with growth.

M2 Money Supply Growth

While there was a recent bottoming in the annual pace of growth, the rebound has remained below median for the money supply. Still, that is growth, it is just not enough to really perpetuate the economy into new highs.

Both personal incomes & expenditures, as well as the rate of growth of the M2 money supply are a push and pull indicator.

If the money supply is growing at a faster pace than previous, this means firms are investing and taking on debt in order to do that—you see this in a fractional banking economy.

When you start to pair both money supply growth as well as incomes & expenditures, there is more of a picture forming.

Oil Prices Are Surging

With 20% of the world’s supply flowing through the Straight of Hormuz, the War with Iran has the potential to be devastating to world economic growth if the straight is left closed for an extended period of time. This will also add to overall price pressures in the United Stated, despite the US being the world’s largest supplier of oil.

PCE Inflation

Interest rates are going to have to remain higher for longer, if not go even higher. I had said previously that I believed the Fed should never have lowered interest rates previously, that the target had not been met. Without the war, price pressures were already heading upward and that needed to be addressed with more restrictive measures.

I look like I may be proven correct, but the Fed moved despite what I believed to be true.

Trump is still hell-bent on tariffs using any means necessary, and that has proven to be inflationary. This is simply more fuel for the fire.

AI Prediction

I am still short my SPY ETF vertical call spread, which expire this Friday—they are worth all of $0.01 now, and I might as well let them simply evaporate to zero. I had been short the vertical puts, and took profits—obviously too early. I attempted to get back in on a short rebound, but my orders never got filled.

From this point, any moves higher in the S&P 500, and I would sell more calls and buy more puts—ceteris paribus… all else equal. If the war in Iran takes a positive turn, that trade idea would die fast.

The real thing I am watching, which I mentioned at the top, is the Treasury yields on the 10. Higher oil prices are going to do no favors for an already-increasing inflation report.

Looking at the 10, I wonder what AI believes:

The Inquiry

The BEA released the latest personal incomes, personal expenditures, and the PCE Index. Annual growth rates are declining for incomes and expenditures, while increasing for price pressures on the core reading. The numbers are far from showing stagflation, which I do not believe we are at the beginnings of. However, the war with Iran has potential to elevate prices further, and that would force the Federal Reserve to increase interest rates if inflationary pressures continue to move higher.

For ow, the US 10-year yield is well entrenched around the 4.28% level, albeit it shot upward from a recent low of about 3.89% just immediately prior to the US launching its attack against Iran.

With slowing growth in the M2 money supply, slowing employment growth, and declining personal income growth and personal expenditure growth, continued increases in price pressures from tariffs as well as newer price increases from higher gas prices will be a strain on growth potential with revenues from companies in the S&P 500.

What can you find with regard to the future outlook of personal income growth, the money supply growth, and how that may affect the Federal Reserve’s position, along with the stock market’s take on future growth rates, along with the potential for higher price pressures? How does this all play out with regard to aggregate demand and revenue growth for S&P 500 components along with what may happen with interest rates and the yield curve?

The Response

What the forward outlook implies (income growth, M2, Fed stance, equities, demand/EPS, curve)

You’re describing a very plausible near-term mix: cooling nominal growth (income/spending/jobs) alongside sticky-to-rising marginal price pressures (core + tariffs + energy). That mix doesn’t have to become stagflation to be a problem for margins and multiples—especially at elevated equity valuations.

Below I’ll anchor to what’s available on the forward outlook from major macro/market outlook sources and then translate it into aggregate demand → S&P 500 revenue/EPS → rates/curve.

What sources are implying about growth/income, money conditions, and inflation risk

Several 2026 outlooks expect continued expansion without an imminent recession, but with volatility driven by supply shocks and policy uncertainty (including tariffs) — e.g., JPMorgan 2026 outlook (PDF), Ameriprise 2026 market & economic outlook, Transamerica 2026 market outlook, James Investment 2026 outlook.

Long-horizon assumptions (not tactical, but informative for “trend”): Schwab’s expectations show inflation settling above 2% on average (sticky), consistent with your point that the “last mile” to 2% is hard: Schwab long-term capital market expectations.

On tariffs: estimates emphasize price-level effects and distributional impacts (inflation impulse + demand drag) rather than clean “growth positive” outcomes: Yale Budget Lab – tracking economic effects of tariffs.

On “where markets think growth/EPS goes”: several sell-side targets embed meaningful EPS growth and relatively high multiples; that’s a setup where any growth disappointment matters more: Investing.com analyst consensus discussion, plus general bank outlooks like JPMorgan 2026 outlook (PDF).

With that backdrop, here’s how I’d frame the next ~6–9 months mechanically.

1) Future outlook for personal income growth & demand: “cooling but not collapsing”

Even if YoY income and spending growth are easing now, most mainstream outlooks still assume modest real growth continuing rather than a sharp contraction (soft-landing base case): Ameriprise 2026 outlook, JPMorgan 2026 outlook (PDF).

How that translates to aggregate demand:

If nominal income growth slows and gasoline/tariff-driven prices rise, the near-term hit shows up as real purchasing power compression, usually:

Lower discretionary goods demand

“Trade-down” behavior

A shift toward essentials/services

That tends to keep top-line revenue growing nominally (prices help) while unit volumes soften.

So your intuition is right: you can get revenue resilience with margin pressure.

2) Money supply growth outlook: positive but not “reflationary turbo”

I’m going to avoid claiming a specific forecast number for M2 from these sources because most “outlook” reports don’t forecast M2 directly in a consistent way. Practically, what matters for markets is whether money/credit conditions are:

Re-accelerating (risk-on, easier)

Flat (range-bound)

Tightening (risk-off)

Given the broader outlooks expecting continued expansion and some easing (not tightening), the implied baseline is: no major credit contraction, but also not a return to 2020-style liquidity.

In your framework: M2 slowing + jobs slowing argues for disinflationary growth, but tariffs + energy reintroduce cost-push inflation.

That is a tricky combo for the Fed.

3) How this affects the Fed: the “cuts are conditional” regime

Multiple outlooks point to the Fed being able to ease somewhat in 2026, but with inflation risks limiting the pace: JPMorgan on Fed rate cuts, iShares Fed outlook / rate forecast framing.

Your setup (slower growth + higher headline/cost pressures) pushes the Fed toward:

Less urgency to cut if core is sticky/rising

Willingness to look through energy spikes if they believe they’re temporary

But if tariffs/energy feed into services inflation/wages or inflation expectations, they can’t ignore it

So the Fed’s reaction function becomes:

“We can’t cut unless growth weakens enough to dominate the inflation impulse.”

That’s why you can have contained 10Y yields even as risk assets wobble: markets price growth risk while the Fed stays cautious.

4) S&P 500 aggregate demand & revenue growth: nominal ok, real/margins at risk

A useful way to think about S&P revenues is:

Nominal demand drives reported sales

Real demand drives volumes and operating leverage

Input costs (labor + energy + tariffs) drive margins

If tariffs/energy lift prices while incomes/spending growth cool:

S&P top-line can look “fine” (inflation helps revenues),

but:

consumer-facing margins get squeezed (cannot pass through fully),

industrials face input costs,

and the “multiple” (P/E) can compress if rates stay high.

These outlooks commonly still embed decent EPS growth (often double-digit), which increases the market’s sensitivity to any earnings revision cycle: Investing.com consensus discussion, JPMorgan 2026 outlook (PDF).

Implication: the market can tolerate “some” cost-push inflation only if:

pricing power holds, and/or

productivity offsets costs

That’s where AI/productivity narratives matter to index-level margins.

5) Rates and the yield curve: competing forces → likely more steepening, but with volatility

Several outlooks expect continued curve normalization/steepening as short rates drift down more than long rates, while deficits/inflation risk keep the long end from collapsing: Transamerica 2026 outlook, James Investment 2026 outlook.

Given your facts:

If energy/tariffs lift near-term inflation prints, long-end yields can remain sticky (term premium).

If growth slows (income/spend/jobs cooling), the front end can price eventual easing, steepening the curve.

So the near-term likely set is:

Range-bound but volatile 10Y

Curve steepening bias (cuts priced in later; long end anchored by term premium)

6) How this “plays out” (probability-weighted scenarios)

Here’s a clean 3-scenario map for the next ~6 months:

Scenario A (Base): Soft landing + cost-push bumps

Income/spend growth slows but stays positive

Core inflation sticky; headline jumps on energy

Fed pauses; cuts delayed

Equities: choppy, selective; earnings revisions modestly down

Curve: mild steepening

Scenario B: Growth scare dominates

Consumers retrench; earnings revisions fall

Fed becomes more dovish despite tariffs/energy

Equities: drawdown, then recovery on “Fed put”

Yields: down; curve steepens more

Scenario C: Inflation re-accelerates meaningfully

Tariffs/energy feed into broader core/wages

Fed signals tighter-for-longer (or hikes)

Equities: multiple compression; leadership narrows

Yields: up at the long end; curve can re-flatten

Tariffs are a key swing factor here, and Yale Budget Lab’s work is directly relevant because it highlights the price-level impulse as a central channel: Yale Budget Lab – tariffs.

My Take

I simply do not see any pathway forward for a rally in the stock market, assuming continued fighting with Iran. Even without the war, inflationary pressures are mounting, which I have been saying would occur for about 18 months now. While I have been playing a lot of theta trades, I am gearing up for a bigger move to the downside with the stock market as the economy slides nearer to a zero-growth landscape.