Trump Lost - Buy Crypto

Iran has an outsized upper hand in the war, and with the new blockade, this could backfire spectacularly. Iran's choice of using crypto for payment could have a supporting effect.

The administration is resorting to having Melania bring up the files so nobody pays attention to the war—it’s getting that bad. In the meantime, developments are still likely to occur sooner rather than later.

The Strait of Hormuz is still closed, but now it is the United States that has done the closing. This is in violation of international law, which that may come back to haunt the administration at a much later date—they are doing it anyway.

Any vessel passing through the Strait has to do so in Iranian waters, and they are more than capable of charging a fee to do so, as per international law. That, however, doesn’t work for an administration that wants desperately to feel as if they are winning something—they are not.

It may be that paying for passage is a new thing, and a permanent thing. There are some 17 million barrels of oil that flow through the Strait in normalized times. That would be about $17M in potential revenue per day for Iran.

More likely than not, however, many countries would get a pass on this and the only countries that would have to pay for passage would be those that Iran might want to pressure the most. I can’t imagine China having to pay for anything, nor maybe India. Instead, think European countries, and having pressure build on those countries would have the most effect.

Given that, maybe this is about 5M barrels a day that are affected by the Iran tax? This would mean a constant flow of having to purchase crypto, and BTC may be a likely candidate. While I do not necessarily see this as a turning point for crypto currencies, it is one more thing to add to potentiality.

Another thing I wonder on is if this could be the beginning of the end of petrodollar hegemony—it is possible to see a shift, and all of a sudden using actual dollars starts to decline. This is another thing that would be a self-inflicted wound. If it did occur, however, it would take years. In the meantime, this is yet another subtle shift for crypto.

The Impact

Oil prices popped at the open in Asia on Sunday after the announcement of the US Navy blockade. Along with that, stock futures fell sharply in Sunday trading. All of that reversed—as almost nobody could have predicted.

Eventually, this will get sorted out. In the meantime, however, this is the biggest supply shock in world history. Europeans are feeling this more than any other region, as the above photo shows (via Yahoo Finance newsletter).

The United States is a net exporter of oil, so while prices have increased, there are no real reports of shortages as of yet.

Energy stocks continue to rise, and I can see this as a solid play. Input costs to US producers have not changed whatsoever from February 27th to today. The only thing that has shifted is the price of oil, and new potential demand from other areas of the world where the shortages have had an effect. Those regions that are not able to get their normal flow are bidding up for remaining limited supplies, which is why spot prices have been driven up as they have.

Eventually, the Strait will be reopened, and the supply shock will dwindle. This will take time, however, and it may be years for the market to get back to its previous equilibrium level of supply & demand, and price of sub-$60 for WTI.

Demand Destruction

I believe this is the beginning of a lot of demand destruction with oil, and yet again, this is a self-inflicted foot-shooting. The phrase “demand destruction” has been bantering around a lot lately because of the conflict. I have heard it being somewhat incorrectly used, however, and I wanted to put out an example of how this all plays out.

The only way demand destruction would occur is if someone who is in the market to buy a new car opts for an EV, and demand for EVs rises above a normalized trend. From that point forward, that individual would no longer “demand” oil because they are using an alternative method of transportation. If enough people do this, that could be noteworthy for the oil industry. I expect this to happen, actually, but I am nowhere near betting the farm on this: this will take years to play out.

It is important to note that someone selling a truck they have owned for a long period of time in favor of a used EV is a smaller example of demand destruction also. Someone will still buy that older truck, and it would get some use which would continue to demand oil. It is the shift from the truck by the original owner to an EV, whether that is their primary vehicle or not, which will add to the demand destruction of oil.

If the price of oil stays high for too long, many individuals will shift their purchase of new vehicles to hybrids or full EVs. There will be a tipping point where a crucial level finally hits. I believe this is the beginning of this, and the world will look backwards on these events as that point in history where mankind was driven off of oil dependency to alternatives.

Interest Rates & Inflation

Interest rates remain elevated, and this will likely continue. Inflation data released last week shows continued pressures upward from the tariffs. With gas prices up some 30% across the world, inflation will work its way back upward once prices trickle through with the increases.

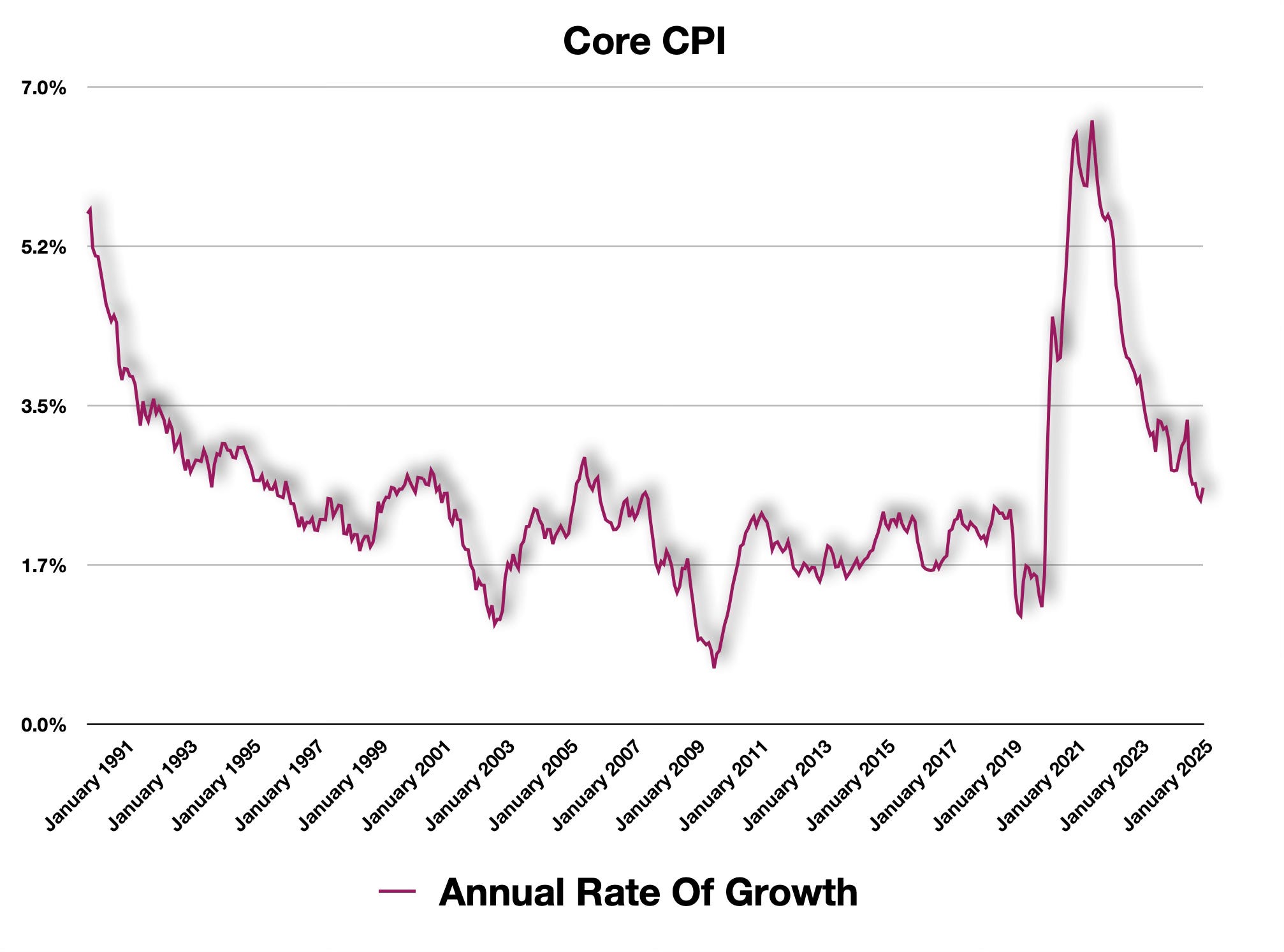

For CPI data last week, the core reading came in at 2.595%, up from 2.475% for annual growth rates. While there was a dip in inflation over the past few months’ data, the most recent numbers have been trending upward again. The moves upward are slight, but they are there.

The Fed will have to hold for some time until they get a solid read on what is happening from the price increases for petroleum products, along with the current effects of tariffs on prices.

Stock Market

Who could have guessed this week would see all-time highs looking like they will get printed again while at the same time, there’s a blockade on oil?

I have a difficult time with this because the consumer, the ultimate driver of the economy, is getting zero relief. While the tariffs had been struck down, the administration found other avenues. Add into this, the rising costs of gasoline at the pump, and the consumer is stretched. With the Fed likely to keep interest rates at firmer levels until price pressures abate to levels that are within target range, and the consumer is being taxed everywhere—this is not the recipe to a booming economy.

Stocks Versus Money Supply

I keep my eye peeled toward the rate of growth for M2, and it is stuck at below median levels. In all honesty, the consumer has held up well, albeit they’ve been constrained with potential.

If the consumer was able to pay less at the pump, if the tariffs simply went away, and if the Fed could lower rates, the economy would have a lot of potential. While I can see lower prices than where they are at the pump, this will be a long, slow drop back downward, and I believe it will take a long time before there’s any moves lower below previous levels—the consumer is simply going to have pay more for the same product than it did prior to the war.

Buy Crypto

Iran has the upper hand I this war. Trump & Co. are desperate for some kind of victory to declare. I would not be surprised if the negotiations end with Iran keeping their sovereign powers in a manner in which they are also charging a fee for passage. With the administration blockading the Strait, it simply keeps oil from flowing, which will pressure US allies into pushing for the blockade to be removed. This war has not accomplished anything of substance, and the administration can only hope for some kind of way out.

In the meantime, crypto currencies have been trending upward on the news that Iran is allowing passage for a fee via crypto. While this is a drop in the bucket, it could be the beginning of something far bigger over a greater period of time.

AI Prediction

Last Friday, I purchased both a long-dated vertical call spread and put spread instead of my usual one sided position. I felt we would see movement, and I felt it would be a solid move. I had zero clue which direction, however, considering the constant changes and shifts. While the calls are doing well, I’m not entirely profitable because of theta. I will begin the process of selling short-dated vertical call spreads against my current position to bring in premium on the short end.

In the meantime, the big rally in the broader stock market is a bit of a surprise—I wonder what AI believes could be next after this?

The Query

Currently, there is a blockade of the Strait of Hormuz by the United States Navy. First, while there is a cease-fire between the US & Isreal versus Iran, the war had not gone well overall for the United States. Now, it appears as if the administration is kinda desperate for some kind of victory, and the blockade appears more helpful for Iran than the United States. In the meantime, the stock market has rallied significantly and oil prices have dropped. Expectations are that there will be some kind of deal, and this will be all over with.

What are your overall thoughts on where the stock market is right now, and how about the prospects for crypto with Iran taxing vessels?

The Response

My take

I think your instinct is directionally right:

The stock market is trading the probability of a deal, not the reality of normalization.

That is an important distinction.

Right now, the market seems to be saying:

the cease-fire is fragile but still meaningful,

the blockade is probably a negotiating lever rather than the start of an unlimited widening of the war,

oil disruption may be serious but temporary,

and corporate earnings outside the most energy-sensitive pockets may still hold up.

That is why stocks have rallied hard even while the geopolitical backdrop still looks messy.

What the market is actually pricing

Recent reporting shows:

the S&P 500 has already erased its war losses and is back near prior highs (AP, Reuters);

oil has pulled back from the worst panic levels, though it is still well above pre-war levels (AP, BBC);

markets are taking comfort from ongoing engagement with Tehran and the idea that a deal is still possible (Reuters, CBS News).

So the market is not saying “everything is fine.”

It is saying:

“Worst-case tail risk is maybe being removed faster than feared.”

That is a much narrower claim.

Why oil has dropped even though the blockade is still in place

This is the key nuance.

Current reporting suggests the U.S. action is not a total sealing-off of all Hormuz traffic. The BBC says Washington is blockading maritime traffic entering and leaving Iranian ports, while ships going elsewhere are supposed to be allowed through the Strait (BBC). Reuters similarly reported that the U.S. was blocking Iran’s ports while talks remained active, and Trump said ships were still passing through Hormuz (Reuters).

That matters a lot.

Because if the market concludes:

this is pressure on Iran’s exports, not a permanent shutdown of all Gulf energy flows,

and talks may resume,

and at least some shipping can move,

then oil can fall from panic highs without the underlying situation actually being healthy.

So I would interpret the drop in oil as:

less fear of immediate catastrophe,

not

confidence that the system is back to normal.

Where I think your skepticism is strongest

You are basically focused on the difference between:

a political off-ramp, and

a physical/logistical recovery.

And I think that is exactly the right place to press.

Even if a deal happens soon, the market may still be underestimating:

damage to Gulf infrastructure,

shipping disruptions and rerouting,

backlog clearance,

insurance and crew risk premia,

mine-clearing / security operations,

delayed restart timelines for damaged facilities.

The BBC notes that traffic through the Strait usually runs around 3,000 ships a month, but fell to just a handful per day during hostilities (BBC). Even if passage resumes more broadly, normal throughput does not instantly snap back.

That means the market may be right on:

headline de-escalation,

while being wrong on:

speed of physical normalization.

So is the blockade “helping Iran more than the U.S.”?

I’d phrase it more carefully:

Strategically/politically, the blockade may be intended to squeeze Iran’s oil revenues and force negotiations (BBC).

Economically, it still keeps a lot of uncertainty in the system and can sustain higher energy prices.

Market-wise, if investors believe it increases the chance of a deal, they may still cheer it.

So the paradox is:

A coercive move can be bullish for stocks if investors believe it shortens the conflict.

That does not mean the move is economically clean or low-cost.

It just means markets are forward-looking and often trade the expected endpoint, not the ugly middle.

Why stocks can rally while the macro setup still worsens

This happens a lot in war / commodity shock episodes.

Equities often bottom and rally when:

the worst-case path becomes less likely,

participants fear missing a peace/deal squeeze,

and oil stops accelerating upward.

Reuters quoted Janney saying investors fear being left behind if resolution comes together quickly (Reuters). That is classic squeeze behavior:

underpositioned investors,

tail risk fading,

fast rotation back into cyclicals / tech / broad beta.

But rallies like that are vulnerable if the macro starts to bite later through:

inflation,

weaker margins,

lower consumer spending power,

tighter financial conditions.

My framework from here

I’d break this into 3 scenarios.

1) Bull case: market is basically right

A deal comes together relatively soon.

Iranian export restrictions ease.

Wider Strait traffic normalizes progressively.

Oil keeps fading lower.

Earnings season shows damage is manageable.

The market continues to rip because it successfully “looked through” the war shock.

In this case:

energy stocks may stall,

cyclicals and tech likely outperform,

yields may stabilize or drift lower if inflation fears cool.

2) Base case: deal eventually, but normalization is much slower than the market expects

This is the one that seems closest to your thinking, and honestly it’s the one I find most plausible.

What happens:

cease-fire holds unevenly,

talks drag,

blockade remains a bargaining tool,

traffic partly resumes but not cleanly,

oil stays below panic highs but above pre-war norms,

equities realize the geopolitical crisis is not over, just less acute.

In this case:

the broad market may stop going straight up,

leadership narrows,

energy remains supported,

transports, airlines, chemicals, and some consumer names remain pressured,

inflation expectations stay too sticky for the Fed to get comfortable.

That would be the classic:

not catastrophe, but stagflationary abrasion

rather than immediate collapse.

3) Bear case: the market is badly complacent

The cease-fire breaks down or enforcement expands.

More ships are disrupted.

Gulf ports/facilities stay impaired.

Oil pushes back toward prior highs or above them.

Inflation fears return hard.

The stock rally reverses because it had priced resolution too soon.

In that case, the market would likely have to reprice:

lower EPS,

higher discount rates,

lower odds of Fed easing.

What this means for oil from here

The market seems to be treating the current oil move as temporary scarcity, not a multi-quarter structural shortage. Reuters even noted comments that futures markets appear to be pricing the surge as short-lived (Reuters).

But if physical constraints persist, oil can remain:

below panic peaks,

yet still high enough to damage the macro.

That is the danger zone for equities.

Because the stock market can absorb:

a short spike in oil.

It struggles more with:

oil that stays moderately elevated for months.

That’s when you start getting:

margin compression,

negative earnings revisions outside energy,

lower consumer real income,

renewed inflation concern.

Consensus for the economy

The broad consensus in reporting looks something like this:

If the conflict fades soon, the global economy avoids the worst-case outcome and markets are vindicated.

If high energy prices persist, global growth weakens materially and inflation remains elevated.

The U.S. is relatively more insulated than many import-dependent economies, but not immune.

Europe and Asia remain more exposed to sustained Gulf disruption.

The IMF has warned that continued war and high energy prices raise recession risk (BBC).

So the consensus is not “everything will be fine.”

It is more:

“There is still a path to avoiding disaster, and markets are choosing to trade that path.”

My bottom line

I would summarize it this way:

The rally in stocks and the drop in oil do not necessarily mean the market thinks the situation is good.

They mean the market thinks the probability of a near-term off-ramp is high enough to justify fading the worst-case scenario.

Your concern is that physical repair, shipping normalization, and supply restoration will lag far behind diplomacy.

I think that concern is very reasonable.

So if I had to distill it:

Equities are trading the cease-fire.

You are thinking about the aftermath.

Those are not the same trade.

And in my view, that is exactly where the risk of disappointment sits.

My Take

This was a fairly long response. My take is that the market is misaligned with reality and simply rallying on the probability of the end of the war. In the meantime, while stocks are near all-time highs again, the longterm reality of infrastructure damage and delays in oil being shipped will eventually weigh on the markets. Because of this, I think I will slowly bring in more short positions against the market.