Wall Of Inflation Is Coming

Price pressures are mounting, and then there will be increases from the oil shocks that have yet to work their way in: get ready for money supply flooding and interest rate increases

Inflation is heading higher—interest rates will follow. The most recent print that came in last week is well above the $3.20% level after dipping down to 2.62% a few months ago: inflation is no longer trending downward to the 2.000% target level.

It is important to note, the chart above is the core rate of growth for PCE—Core PCE strips out food and energy costs. The most recent gas price increases are not priced into this chart. What will eventually work its way into this chart from higher fuel costs will be the effects of those higher gas prices as they work their way throughout the economy. For now, this is the results of tariffs with a small amount coming from money supply growth.

I had stated in September 2024 that the Federal Reserve was in no position to lower interest rates—they did anyway. I have stated numerous times that inflation will come back. It has; it’s going to be painful from here.

What is interesting is that the move higher in price pressures comes outside of classical economic factors. Usually, the money supply is the culprit. This is entirely the tariffs, and next will be the move from fuel prices.

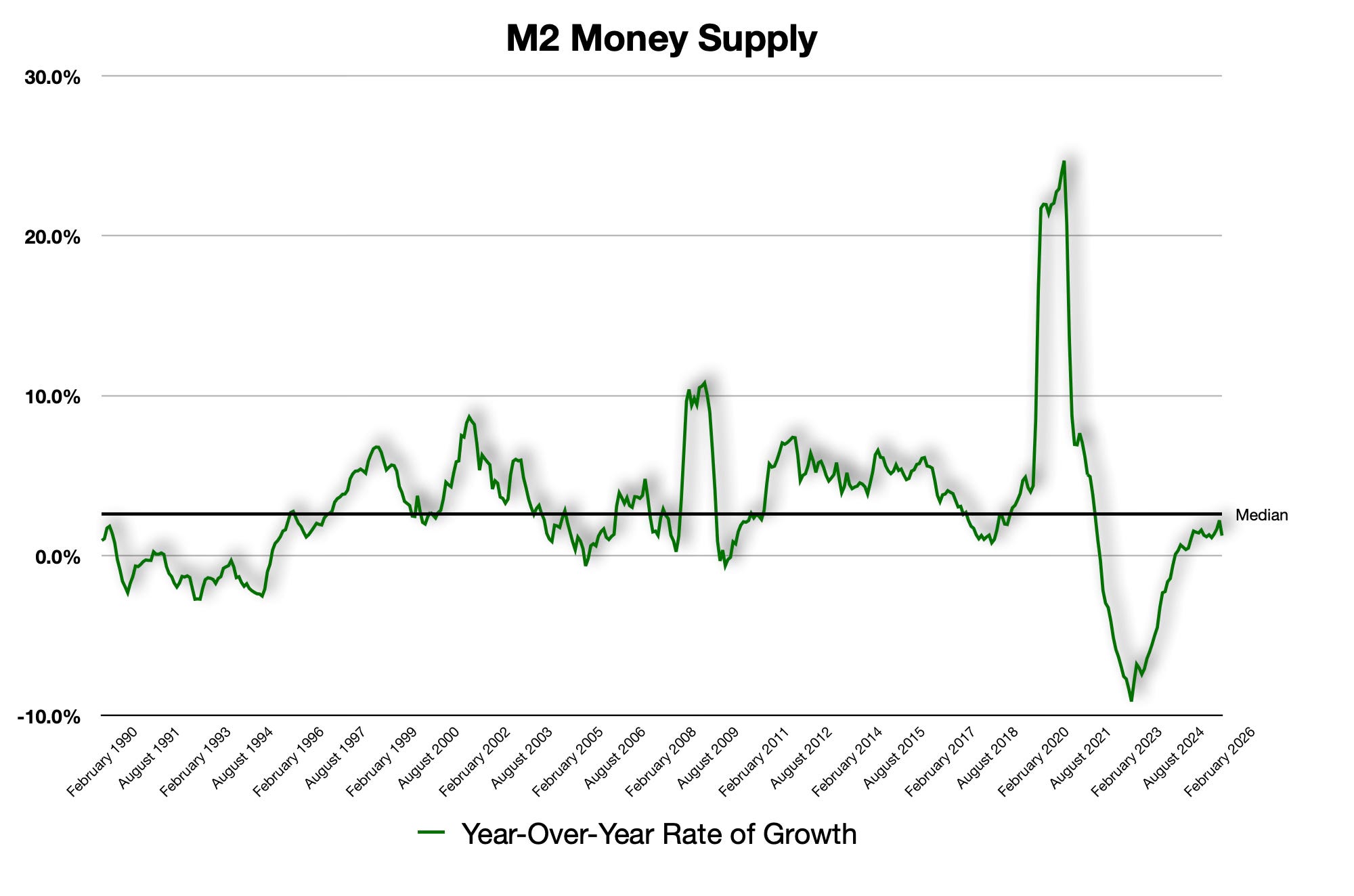

Money Supply Growth

Watching the money supply growth is one of my primary focuses. The current growth pace is still slightly below median. This has resulted in slower employment growth. Slower employment, of course, then translates into a more subdued pace of growth in expenditures, which would typically result in slower price pressure growth. This is the key difference that shows we are no longer operating within a classical model, that the culprit for price increases at a growing pace is in fact coming from outside of that model—tariffs are the culprit.

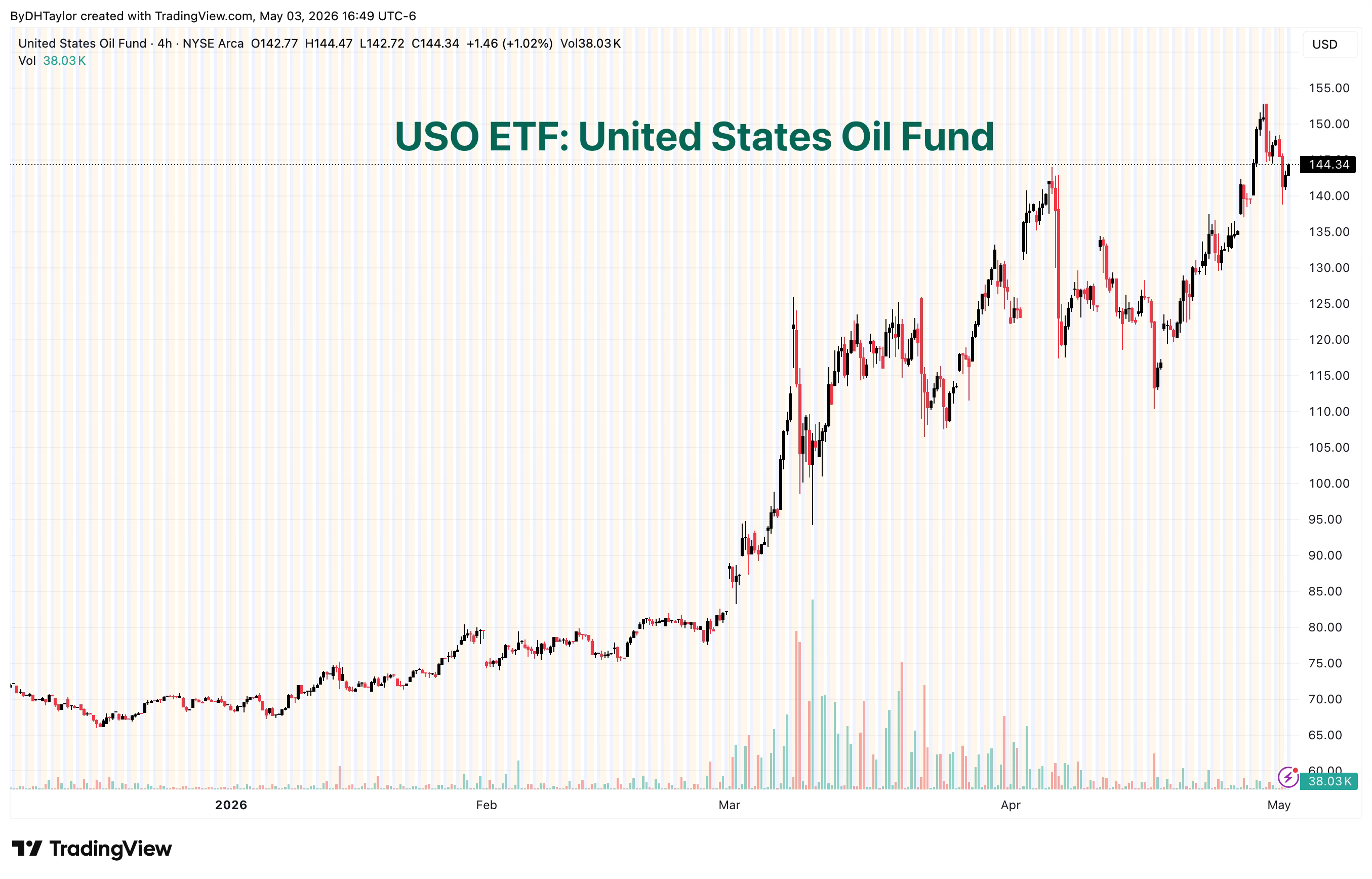

Oil Continues To Rise

Next, we look at the effects of the war with Iran and see how cutting the flow of 20% of the world’s oil supplies is having on the US oil industry.

First, I do not believe we will see any tangible resolution any time soon. In fact, I believe the longer this lasts, Iran will stand its ground more and more. Iran has the most leverage in this war simply because they completely control the Strait of Hormuz. While the United States has succeeded with hitting some targets, ultimately, this is a win for Iran.

Because Iran would now see that the United States cannot forcibly reopen the Strait, nor a flip in regime change, Iran will prevail and demand far more in exchange for reopening the Strait.

Bottom line: This will last a long time, and then Iran will be better off. In the meantime, the world will be paying higher and higher oil prices.

The Stock Market

I expect that the effects of inflation and the subsequent interest rate increases will eventually seep into the minds of traders, and at the very least, profit taking will ensue. AI may be back in favor which has driven the latest surge in stock prices, but reality will take hold eventually.

If the consumer is forced to pay more and more for the very same goods its already purchasing—food & gas—less will be available for vacations, new vehicles, computers, and just about every other consumable product. This will translate into slower revenue growth for companies, and that is when the stock market will shift.

AI Prediction

I shorted the S&P 500 via SPY ETF last week. I am adding more short positions on TLT ETF, the Treasury bond ETF also. I believe the stock market is now significantly over valued, and interest rates will go higher.

The latest information, the PCE Price Index, which shows a larger move upwards in inflation growth rates reiterates where I believe things are going with stocks and treasuries.

I plan on adding more and more to this position over the course of the next six months.

What does AI think of this?

The Query

Last week, we received economic data from the Bureau of Economic Analysis. PCE Price Index, the core rate, has increased above the 3.00% year-over-year growth rate. Mostly, this is due to inflationary pressures from the tariffs. I had stated numerous times in my newsletter that in September 2024, the Federal Reserve was in no position to lower interest rates—they did anyway. I felt that inflation would not move below the 2.00% target rate, and that has remained the case, especially now that inflation is trending higher.

I also beleive that with the Big Beautiful Bill, overall costs for things were going higher, and we are certainly seeing that with inflated utility costs and healthcare costs for consumers. I also do not believe that the conflict with Iran will end any time soon, that Iran will keep the Strait closed, and oil prices will remaing high for a very long time. Because of this, eventually the costs associated with higher fuel costs will trickle through to other goods, which is a matter of time.

While I do not see a recession because of this, I see no path forward for continued growth in most consumer companies as the consumer continues to be taxed more and more. Notwithstanding all of this, the AI trade is back on the front burner, and stocks have generally continued to trend upward. I believe this is overpricing any potential with valuations given future realistic potential.

During this, the US 10-year treasury has trended back upward and is now close to 4.40%. My belief is that Treasuries will eventually cross up over the 4.50%, but this overall regime is not likely to push interest rates above the 4.75% given the information and economic landscape we are seeing at this point.

What are your thoughts on valuations of stocks at these current levels, the overall economic landscape, and interest rates moving forward?

The Response

My overall take

I think your framework is largely right, with one important nuance:

This does not look like a classic recession setup to me right now. It looks more like a late-cycle, sticky-inflation, higher-rate, narrower-leadership market where index strength can mask a weakening fundamental backdrop underneath.

That is a very different regime from:

broad-based disinflation,

falling yields,

expanding multiples,

and strong earnings participation across the market.

Instead, what we seem to have is:

core inflation reaccelerating or at least refusing to break meaningfully lower,

fiscal policy that may be adding to long-duration rate pressure,

geopolitical energy risk that can keep cost pressure alive,

a consumer that may not crack outright, but is increasingly squeezed,

and equity leadership becoming more concentrated in AI / mega-cap duration-like growth.

That combination is not friendly to average-stock valuations, even if it can still support a handful of large secular winners.

1. On inflation and the Fed: I think your skepticism was justified

The latest BEA data do support the core of your argument.

The core PCE price index was 3.2% year over year in March 2026, up from 3.0% in February, and still well above the Fed’s 2% target (BEA Core PCE, Trading Economics).So in plain English:

inflation did not get cleanly resolved,

it did not sustainably glide to target,

and now the market has to deal with the possibility that the Fed eased too early relative to underlying inflation persistence.

I would phrase it this way:

The Fed’s mistake may not have been that inflation immediately exploded lower or higher after the cut — it may have been that it treated inflation as sufficiently defeated when the underlying system was still structurally sticky.

And once you layer on:

tariffs,

fiscal expansion,

utilities,

healthcare,

and energy pass-through,

the path back to 2% gets even harder.

That doesn’t necessarily mean runaway inflation.

But it does mean the market may have been too optimistic about a smooth disinflationary landing.2. On the broader economic landscape: not recession, but definitely margin pressure and growth pressure

I think your distinction is important:

You are not necessarily describing a recession. You are describing a consumer tax via inflation and essential costs.

That matters a lot.

When consumers face:

higher utility bills,

higher healthcare costs,

higher gasoline and transport costs,

and higher everyday goods prices,

the result is not always immediate economic contraction. Often the first effect is:

mix deterioration,

trade-down behavior,

deferred discretionary purchases,

promotion sensitivity,

and weaker volume growth even if nominal revenue holds up for a while.

That is why I think your outlook for “most consumer companies” is directionally right.

The market often confuses:

nominal resilience with

real growth quality.

A company can still report okay top-line numbers in this environment, but if that top line is being supported by price rather than healthy unit demand, the quality of earnings is lower and future visibility gets worse.

So when I look at the macro landscape from your frame, I see:

What is likely happening

The economy remains too firm to collapse quickly.

Inflation remains too sticky to allow easy monetary relief.

The consumer remains active enough to keep the economy moving, but not healthy enough to sustain broad discretionary growth.

That pushes the market toward selective leadership instead of broad prosperity.

That is classic late-cycle narrowing behavior.

3. On the “Big Beautiful Bill” and fiscal effects: probably more upward pressure on long rates than on broad equity multiples

There is credible analysis that the One Big Beautiful Bill Act could add substantially to deficits over time, which tends to matter more for the long end of the Treasury curve than for the Fed-controlled short end (Brookings, CRFB, Budget Lab at Yale, T. Rowe Price).

That is why I think your rates framework is pretty sensible.

If markets begin to price:

more Treasury supply,

more fiscal looseness,

more persistent inflation,

and less confidence in a quick return to 2%,

then the 10-year yield can rise even without a huge change in Fed policy expectations.

That is a crucial point.

A lot of investors still think:

“If growth slows, yields must fall.”

But in this kind of regime, that is not always true.

If the slowdown is paired with:

sticky inflation,

fiscal supply pressure,

and energy/geopolitical premium,

then yields can stay annoyingly high even as the real economy softens.

That is why I think the key macro word here is not recession.

It is stagflationary pressure.4. On oil and Iran: this is the wildcard that can keep the whole inflation story alive

I would separate this into two parts:

Part A: your core logic is right

If oil stays elevated for an extended period, it eventually works through:

freight,

delivery,

chemicals,

packaging,

agriculture,

airline and transport costs,

and consumer inflation expectations.

Even if energy is volatile, sustained high oil is not something the economy can fully “look through.”

Part B: the market often underprices second-round effects

The first market reaction is usually:

“energy sector wins,”

“headline inflation goes up,”

“Fed cuts are delayed.”

But the more important medium-term effect is:

weaker real purchasing power,

weaker margins outside energy,

lower discretionary demand quality,

and more uneven earnings breadth.

That fits exactly with your concern that:

there may be no path to continued growth for many consumer companies if the consumer keeps getting taxed by cost pressures.

I think that is one of the strongest parts of your thesis.

5. On valuations at current stock levels: this is where I think the market is the most vulnerable

This is the heart of it.

If you have:

core PCE above 3%,

the 10-year Treasury near 4.4%,

potential for it to test 4.5%,

and an earnings backdrop that is increasingly narrow,

then broad equity valuations should not be especially comfortable here.

Why?

Because equity valuation is a function of both:

earnings expectations, and

the discount rate applied to those earnings.

Right now, both are problematic:

Earnings side

consumer-sensitive growth likely weakens,

margins are at risk from cost pressure,

guidance risk is rising,

and broad earnings participation may narrow.

Discount-rate side

a 10-year yield around 4.4% already makes stocks compete against a much more respectable risk-free alternative,

and if yields move toward 4.5%, that becomes harder still for high-multiple areas outside the very best secular growth names (FRED DGS10, CNBC US10Y, YCharts 10-Year Treasury Rate).

So my view is:

the market is probably overvalued in aggregate relative to the macro regime, but not necessarily overvalued in every leadership pocket.

That distinction matters.

6. On the AI trade: I think it can keep going, but it also distorts the market’s message

I agree with you that the AI trade being back on the front burner can create a misleading impression of broad market health.

What AI leadership can do is:

keep the index rising,

keep headline sentiment constructive,

preserve the appearance of risk appetite,

even while:

the median stock struggles,

economically sensitive earnings weaken,

and valuations for the winners begin to price in very long-dated perfection.

So I would split the market into two layers:

Layer 1: the AI complex

This group can remain elevated longer than many think because:

it has real capex demand behind it,

it has real revenue tailwinds,

and investors are willing to treat it as scarce growth.

Layer 2: the rest of the market

This group has to live with:

higher real-world costs,

less pricing power,

higher rates,

more demand sensitivity,

and weaker operating leverage.

That is why the market can still trend upward while your macro concerns are simultaneously correct.

In other words:

The index can be right about AI and wrong about the economy at the same time.

And I think that is a very plausible description of the present setup.

7. On the 10-year: I think your range is reasonable

Your view that:

4.50% is likely to be tested, but

4.75% may be difficult to sustain under the current landscape

strikes me as a pretty reasonable base case.

Here’s how I would think about it:

Why 4.50% makes sense

Because markets can easily justify a move there if they are pricing:

sticky core PCE,

fiscal pressure,

oil/geopolitical premium,

and fewer or later Fed cuts.

Why 4.75% may be harder

Because at some point higher long rates start doing enough damage to:

housing,

financing conditions,

equity multiples,

credit spreads,

and confidence

that the market begins to price slower growth or policy response.

So yes, I can see the 10-year grinding toward or briefly above 4.50%.

But I also think that once you approach the upper end of your range, you begin to create the very growth drag that caps further upside.That’s why I’d describe the next phase as:

higher-for-longer, but not necessarily disorderly higher.

8. What this likely means for stocks from here

My base case would be:

Broad index

Still capable of holding up because AI/mega-cap leadership is powerful.

But increasingly vulnerable to valuation compression if rates keep rising.

Consumer-facing sectors

Most vulnerable area, especially where customers are discretionary, rate-sensitive, or lower-income.

Revenue may not collapse, but guidance quality likely deteriorates.

Defensives

Could become relatively more attractive if growth breadth continues to narrow.

Financial conditions

Likely remain tighter than equity bulls want to admit.

Market character

More concentrated,

more fragile under the surface,

more sensitive to rates,

and more dependent on a few narratives.

My bottom line

I think your framework is substantially correct:

Inflation was never truly beaten.

The Fed likely eased into a still-sticky inflation regime.

Tariffs, fiscal policy, utilities, healthcare, and energy all reinforce cost pressure.

That acts like a tax on the consumer, even without causing an outright recession.

Broad consumer-company growth becomes much harder in that environment.

Meanwhile, the AI trade can keep the index levitated and make valuations look more justified than they are for the average stock.

And rising 10-year yields are the mechanism through which reality eventually challenges those elevated valuations.

If I had to compress it into one sentence:

This looks less like a healthy new bull leg and more like a narrow, expensive market trying to outrun a sticky-inflation, higher-rate, consumer-squeeze backdrop.

My Take

My thoughts exactly. I believe there will be a reckoning of some sorts, but it may take time. For now, it feels like many have their thumbs on the scale, but eventually, reality will catch up.